Precision Drilling Corp. was aiming for Bone Spring in the Delaware Basin in this file photo.

Learn more about Hart Energy Conferences

Get our latest conference schedules, updates and insights straight to your inbox.

In the glitzy urban centers of Texas, people like to joke that far West Texas beyond the Pecos River is not the end of the earth—but you can sure see it from there. However, that perception has changed lately. Energy investors now view the scrubby, remote region with a much more positive eye—and in many cases, a wide-open check book.

Seemingly overnight, the Delaware Basin has become the hottest petroleum province in the country in terms of ever-higher acquisition prices, and even more remarkably, drilling success on a grand scale, thanks to Apache Corp.’s recent Alpine High discovery in Reeves County, which could change the face of West Texas. Apache said it could recover billions of barrels of oil equivalent (boe) from 4,000 to 5,000 feet of stacked pay.

The Delaware Basin’s appeal—and cost of entry—has been building since 2010, when Concho Resources Inc. paid $1.6 billion for Marbob Energy Corp.’s New Mexico assets and Apache paid $3 billion for BP’s assets in West Texas and southeastern New Mexico. Horizontal drilling and new fracturing practices began to unlock new reserves. The appeal was further highlighted in August 2015 when WPX Energy Inc. acquired RKI Exploration & Production LLC’s assets there for $2.75 billion. The deal gave WPX 10 or 12 prospective benches in a 9,000-foot, hydrocarbon-charged stratigraphic column that includes the Wolfcamp Shale, Bone Spring, Avalon and Delaware sands.

Although several multibillion-dollar acquisitions have caused a stir in the nearby Midland Basin as well, the Delaware now competes for the title of strongest play around.

“The cat is now officially out of the bag that the Delaware Basin is strong to quite strong, and the impact on A&D valuations, as well as grassroots leasing efforts, has become evident,” wrote Seaport Global Securities’ analyst Mike Kelly this summer. At the time, he had just visited with several E&P companies active in the basin, including Luxe Energy LLC, which told him the difference in the basin now was like “night and day” from a year ago. Core risked Delaware acreage was going for $30,000 earlier this year but has trended up since then toward $45,000 an acre.

NGP-backed Luxe turned out to be a fast mover. In January it touted its entry into the basin when it bought undeveloped acreage in Reeves and Ward counties from two private sellers. It cited the allure of several thousand feet of over-pressured oil column, but by September it had already sold the package for $560 million to Diamondback Energy Inc.

Luxe executives had told Kelly they believe the A&D market in the Delaware is transitioning to focus more on acreage swaps between the established players. “Furthermore, the increased competition combined with acreage that is already held by production (minimal lease expiration issues), has made a grassroots, organic leasing program nearly impossible to execute,” said Kelly’s report.

In any case, next year the Delaware will remain the “go-to” basin for E&Ps seeking oil inventory growth, by drilling or acquiring, because E&Ps will be refocusing on building resource potential instead of repairing balance sheets, said Subash Chandra, Guggenheim Securities LLC analyst who has studied 1,500 wells in the play.

In a September report titled Delaware Basin Digest, he explained why the region merits so much attention: It’s got legs. Due to the twoyear drilling downturn, the reserve-to-production (R/P) ratio for many E&P firms has declined, he said, which in turn is correlated to trading multiples such as enterprise value to EBITDA (EV/EBITDA).

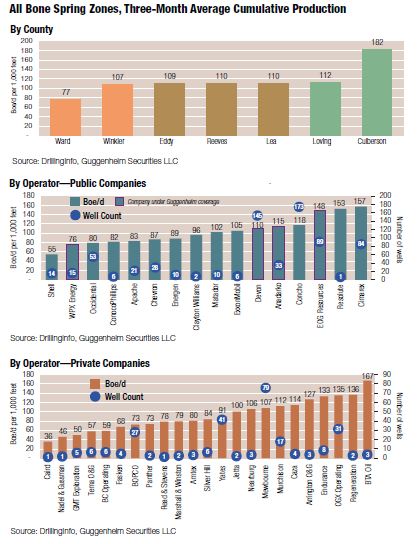

Culberson and Loving counties rank highest for Bone Spring three-month cumulative production per thousand feet of lateral. Dozens of public and private E&Ps are cracking the code in the Bone Spring’s complex zones.

“Acquisitions make more sense to us given the slow pace of exploration, generous equity markets, rapid de-risking of certain intervals of the Delaware Basin, and a flat oil curve that is unhelpful to legacy noncore positions. We believe the Delaware is appealing to all companies, large and small ... We expect it to be as appealing to Shell and Chevron as it is to Resolute Energy Corp. and PDC Energy,” he said.

In fact, there has been a flurry of Delaware deals. In August PDC acquired assets in Reeves and Culberson counties from two private firms, Arris Petroleum Corp. and 299 Resources LLC, for $1.5 billion. It gained approximately 530 MMboe of net reserves based on drilling four to 12 wells per section. That could be an estimated 700 gross locations in the Wolfcamp A, B and C zones.

In October Resolute closed on a Reeves County package for $135 million, enhancing the Permian position it has held since 2011. At press time, Occidental Petroleum Corp. was the latest buyer, announcing a $2 billion spend on Permian Basin EOR assets and 35,000 net acres in Reeves and Pecos counties, the latter bringing at least 700 gross Wolfcamp and Bone Spring locations. (Oxy did not reveal the private sellers or price for the Delaware assets.)

Delaware’s appeal

What are the Delaware Basin’s qualities that lend so much confidence to these operators and buyers? First and foremost it holds a thick wellspring of stacked pay targets in the Wolfcamp A, A X-Y, B and C and three Bone Spring zones, although the area is geologically complex and more work needs to be done. The Wolfcamp A and Bone Spring are already well-established in several areas, Chandra said, and significant potential exists once further de-risking of the Lower Wolfcamp and Bone Spring zones occurs.

Apache’s Alpine High discovery also hints at tantalizing potential in the older Pennsylvanian, Mississippian and Devonian formations. Other possibilities include the Avalon/Leonard and the Blair shales, Chandra noted.

Other analysts also are taking a deeper dive into the Delaware’s attractions. “In our opinion one of the most exciting developments that has yet to get much press is delineation at the Third Bone Spring Shale,” said Seaport Global’s Kelly. “This carbonate zone of the 600-foot thick Bone Spring column ... is deemed to be the same stellar rock that goes by the Lower Spraberry name in the Midland Basin.” If rates of return end up being similar to the Spraberry, the Delaware Basin’s status will rise even higher, he said.

Although acreage in other top plays appears to be close to being locked up, such as in the Scoop/Stack area of Oklahoma, the Delaware is still relatively unconsolidated, Chandra said. This makes it somewhat easier for additional E&P companies to enter or augment their existing positions, despite the increasing deal prices. Public companies in the basin include Energen Resources Corp., Parsley Energy Inc., Clayton Williams Energy Inc., Concho Resources, Matador Resources Co. and Cimarex Energy Co.

More deals could be coming. Several private independents remain active with significant acreage, resource exposure and good well results—Chandra said he counted nearly 20 private E&Ps working in the Delaware. Kelly also cited several private companies: Brigham Resources LLC (65,000 acres), Jagged Peak Energy LLC (with 60,000 acres, it’s rumored to be exploring either a sale or an IPO), Three Rivers Operating Co. (45,000 acres) and J. Cleo Thompson (64,000 acres).

Already this year, some large private operators have made hay out of their Delaware assets: Yates Petroleum Corp. went to EOG Resources Inc. for $2.5 billion, Centennial Resource Development Inc. pivoted from a possible IPO to selling instead to Silver Run Acquisition Corp. for $1 billion (in effect now being public), and Luxe Energy sold to Diamondback Energy Inc. for $560 million.

Although private equity-backed players are taking advantage of the sellers’ market, PE funds still want to be in the basin. In August private equity firm Blackstone Energy Partners unveiled two Permian partnerships by committing an aggregate $1.5 billion to back start-up E&Ps establishing a foothold in the Delaware and Midland basins.

The $1 billion stake was committed to Jetta Permian LP, based in Fort Worth, for its Delaware activity. Earlier in the year, Jetta Operating Co. had sold a small package in Reeves County in the southern Delaware to Concho Resources for $360 million. The second company is Guidon Energy LLC, which is building in Martin County. It is led by Jay Still, formerly the president and COO of Laredo Petroleum Inc. and a top executive at Pioneer Natural Resources Co.

Culberson and Eddy counties rank highest for Wolfcamp three-month cumulative production per thousand feet of lateral. Results are improving steadily in all Wolfcamp zones as completions increase, but plenty of unknowns remain.

De-risking ahead

Apart from the robust deal flow, rapid de-risking by the drillbit is continuing throughout the region, with 10,000-foot laterals becoming the norm. “New operators can enter the Delaware positions confident that one or two zones and intervals within these zones will be productive,” said Chandra.

But after looking at results from over 1,500 wells and from many operator records, Chandra said many unknowns remain across the Delaware. However, he came to some conclusions. On the geology side, the Wolfcamp A is still the most appealing prize for its nature as both reservoir and source rock with lateral continuity, he said. “Loving, eastern Reeves and Eddy counties are desirable for their higher initial production rates and lower gas-oil ratios."

The Second Bone Spring sand seems to be better in Eddy County north of the basin’s slope. In Culberson County, the Upper and Lower Wolfcamp is gassier and the Bone Spring is a more challenging target. The Wolfcamp thins and is shallowest in southwestern Reeves County.

On the technical side, companies still need to figure out the best completion designs. Initial production rates are correlated to proppant intensity, but the amount of fluid used does not seem to correlate with IPs, he found.

Chandra said he thinks operators need to better understand the geology and reduce the variance in well results before routinely increasing proppant intensity, although a great deal of experimentation is going on. “We expect the optimal completion recipe will vary by area. Most of the wells were stimulated with less than the 2,000 pounds per foot that are nearly routine in more developed basins,” he said.

Chandra’s list of remaining unknowns includes the repeatability of the Lower Wolfcamp zone, the potential of the Bone Spring in the southern Delaware, the possibilities in Pecos County and the non-Permian-aged potential as now identified by Apache. Access to water for fracking and water disposal thereafter will also have to be addressed. If the hopes and plans of operators from majors to startups can be gauged by the dollars they’ve spent to enter the Delaware, the basin looks to be well delineated by this time next year.

If the hopes and plans of operators from majors to startups can be gauged by the dollars they’ve spent to enter the Delaware, the basin looks to be well delineated by this time next year.

Recommended Reading

Exxon Mobil Guyana Awards Two Contracts for its Whiptail Project

2024-04-16 - Exxon Mobil Guyana awarded Strohm and TechnipFMC with contracts for its Whiptail Project located offshore in Guyana’s Stabroek Block.

Deepwater Roundup 2024: Offshore Europe, Middle East

2024-04-16 - Part three of Hart Energy’s 2024 Deepwater Roundup takes a look at Europe and the Middle East. Aphrodite, Cyprus’ first offshore project looks to come online in 2027 and Phase 2 of TPAO-operated Sakarya Field looks to come onstream the following year.

E&P Highlights: April 15, 2024

2024-04-15 - Here’s a roundup of the latest E&P headlines, including an ultra-deepwater discovery and new contract awards.

Trio Petroleum to Increase Monterey County Oil Production

2024-04-15 - Trio Petroleum’s HH-1 well in McCool Ranch and the HV-3A well in the Presidents Field collectively produce about 75 bbl/d.

Trillion Energy Begins SASB Revitalization Project

2024-04-15 - Trillion Energy reported 49 m of new gas pay will be perforated in four wells.