Companies are largely selling acreage in noncore areas to pay for development and expansion in core plays, such as the Permian Basin. But others are also making substantial acreage swaps, some valued at hundreds of millions of dollars. (Source: Hart Energy)

Acreage trades lack the splash and big-dollar headlines of most A&D transactions, but it’s clear oil and gas E&Ps like a good old-fashioned swap when they can get one.

Industry players have spent the third quarter—and much of 2017—securing contiguous borders with deals requiring little to no cash but adding what they say is a lot of inventory and a lot of length for lateral wells.

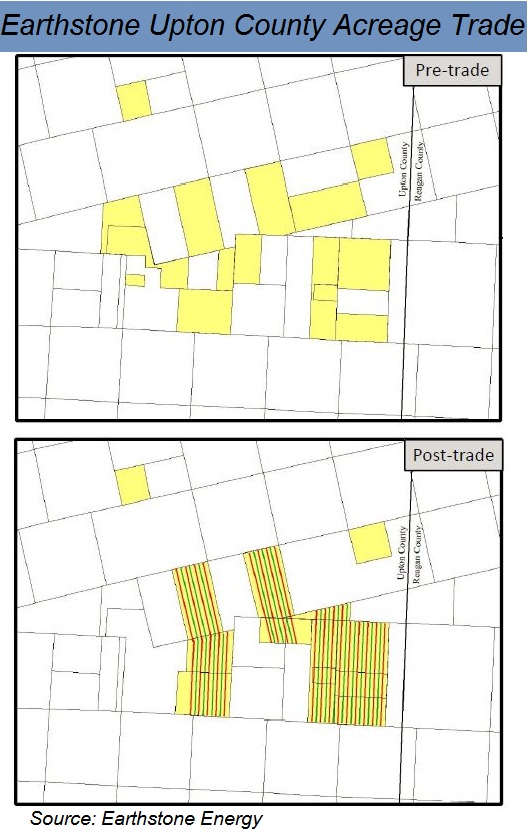

In the Midland Basin, Earthstone Energy Inc. (NYSE: ESTE) was among the most recent to engage in bartering its way to longer laterals without having to fritter away its cash. The company said on Oct. 18 that it blocked up acreage in its Benedum prospect in Upton County, Texas, into concentrated positions that consist of 2,650 net acres, 95% working interest and 80% net revenue interest.

The trade additionally added 62 gross potential drilling locations in the Wolfcamp A, Upper B and Lower B targets with additional upside in the Sprayberry and Wolfcamp C. Average lateral lengths now stretch to 6,550 feet, the company said.

Earthstone wasn’t alone, as E&Ps in the Permian Basin, Haynesville Shale, Wattenberg Field and elsewhere have made similar exchanges. Majors such as Chevron Corp. (NYSE: CVX) also see the most accretive and value-enhancing deals to be made are through trades.

Acreage swaps may reflect what PwC sees as a larger trend among oil and gas deal makers focused on smaller, bolt-on acquisitions rather than budget-busting transformational deals.

In a PWC report released Oct. 26, the firm saw an uptick in deal volumes but a plummet in values in third-quarter 2017. Announced deals rose in the quarter to 53, up 13% compared to the same period last year. Deal values, however, fell 58% year-over-year to $23.61 billion.

In upstream A&D, shale deals remained a major contributor to activity but centered on transactions designed to gain greater economies of scale on existing assets and infrastructure.

Whether the extent of acreage trades and swaps is rising is unclear. In an interview, Joe Dunleavy, PwC U.S. EU&M deals leader, said that analysts identified 18 swap transactions during the past 11 years. Half of the total occurred in 2014, he said.

“Some of this is just based upon the description in the data,” Dunleavy said. “We haven’t really, at least in the past couple of years, focused in on it. Since 2015, there’s only about four that we’ve identified in the data.”

Further, not all trade and swap deals have an announced value, which excludes it from PwC and other firm’s analysis. PwC analyzes deals of $50 million or more for its A&D report.

“If I put it in the context of what we’re seeing now, we’re seeing people getting rid of noncore assets and focusing in on where they have their core business, wherever they define that,” he added.

Earthstone itself following the trend Dunleavy suggests.

CEO Frank A. Lodzinski said the company has sold most small legacy properties to focus Earthstone’s “financial and human capital” on the Midland Basin. The company is now considering a divestiture of its Bakken nonoperated assets, which averaged about 876 barrels of oil equivalent per day in the third-quarter, with about 64% of production oil.

Selling the Bakken assets “would allow us to further support our growth in the Midland Basin,” Lodzinski said. “We anticipate that by year-end we will have streamlined our asset portfolio considerably.”

Overall, 2017 has seen a several shale acreage swaps—many sizeable and in prime areas—that have concentrated on blocking up acreage for longer laterals or cobbling together higher working and net revenue interests.

Values are generally hard to come by, however.

In Weld County, Colo., PDC Energy Inc. (NASDAQ: PDCE) shored up its core Wattenberg Field holdings through a $210 million acquisition and a separate acreage swap, the company said in September.

The value of the acreage trade in PDC Energy’s Plains Area is difficult to calculate. The trade gives away 12,100 net acres in exchange for 11,700 net acres. PDC said in a news release that the difference in the acreage is “primarily due to variances in working and net revenue interests.”

In October, Goodrich Petroleum Corp. (NYSE American: GDP) shuffled around about 900 acres from its Metcalf area in the central area of Caddo Parish, La., for a similar amount of acreage in its Bethany-Longstreet area in southern Caddo.

The upside, Goodrich said, was increasing its longer laterals and operated acreage with lower gathering fees. The deal also equated to an increase in proved, undeveloped reserves of 25.5 billion cubic feet equivalent of natural gas. Following the trade, Goodrich now holds 13,400 net acres in the core Bethany-Longstreet area, Capital One Securities analysts said.

The Permian, however, still gets the most buzz even when dollars aren’t the focus.

In September, Parsley Energy Inc. (NYSE: PE) gave slightly more solid ground. The company said trades added 5,600 premium net acres in the Permian Basin that, by analysts’ estimates, were worth roughly $200 million.

Since its $2.8 billion deal to purchase 71,000 net acres from Double Eagle Energy Permian LLC, the company has been reluctant to engage in more cash-based deals. But Parsley had indicated it isn’t done with swapping acreage, saying earlier in the year it had identified at least 13 opportunities that could equate to $1 billion in acquisitions.

Parsley’s swaps traded the company out of scattered and nonoperated properties with 25% average working interests and into concentrated, operated properties with 85% average working interest.

“Recent trades added more than 500,000 net lateral feet to horizontal drilling inventory, on top of 900,000 net lateral feet previously added following the Double Eagle acquisitions,” the company said. Post Double Eagle trades are “akin to adding 5,600 premium net acres with four target intervals.”

Parsley paid roughly $36,000 per acre for its Double Eagle transaction, giving the traded acreage a ballpark value of $202 million.

Even among the largest oil and gas producers, swaps are seen as lucrative ways to make deals and increase value.

Jay Johnson, executive vice president for Chevron upstream, said in a July conference call that the company is managing its portfolio in the Permian through joint ventures, farm-outs, sales and acreage swaps.

“We have identified between 150,000 and 200,000 acres in the Midland and Delaware basins that we plan to transact to generate more immediate value,” Johnson said. “Generally, the highest value transactions are swaps to core up acreage and enhance value through long laterals and other infrastructure efficiencies.”

Darren Barbee can be reached at dbarbee@hartenergy.com.

Recommended Reading

Sapura Acquires Exail Rovins’ Nano Inertial Navigation System

2024-02-01 - Exail Rovins’ Nano Inertial Navigation System is designed to enhance Sapura’s subsea installment capabilities.

Curtiss-Wright to Deploy Subsea System at Petrobras' Campos Field

2024-02-12 - Curtiss-Wright and Petrobras will combine capabilities to deploy a subsea canned motor boosting system at a Petrobras production field in the Campos Basin.

Subsea Tieback Round-Up, 2026 and Beyond

2024-02-13 - The second in a two-part series, this report on subsea tiebacks looks at some of the projects around the world scheduled to come online in 2026 or later.

AI Advancing Underwater, Reducing Human Risk

2024-03-25 - Experts at CERAWeek by S&P Global detail the changes AI has made in the subsea robotics space while reducing the amount of human effort and safety hazards offshore.

2023-2025 Subsea Tieback Round-Up

2024-02-06 - Here's a look at subsea tieback projects across the globe. The first in a two-part series, this report highlights some of the subsea tiebacks scheduled to be online by 2025.