Big reserves—and getting bigger: That’s the good news about the Marcellus and Utica plays. By some analysts’ estimates, the Marcellus now ranks as the largest natural gas field in the world, ahead of the gigantic South Pars Field that laps over into Iran and Qatar from beneath the Persian Gulf.

And the smaller Utica hardly would rate as little brother anywhere else, except given its nearness to the sprawling Marcellus.

The Potential Gas Committee and the American Gas Association (AGA) released the committee’s biennial update on U.S. gas reserves late in the third quarter, which estimated the nation’s gas resource base at 3,374 trillion cubic feet (Tcf) at yearend 2018.

“This is the highest resource evaluation in the committee’s 54-year history, exceeding the 2016 assessment by about 20%—the largest two-year increase in the report’s history,” the AGA noted.

Drill down in the study and the really impressive number that jumps out is that the report’s Atlantic area—read that Marcellus and Utica—jumped 25% to 1,311 Tcf in two years. The report’s Midcontinent, which includes the Permian Basin, Oklahoma’s Scoop/ Stack plays and the landmark Hugoton Basin in Kansas and Oklahoma, recorded a higher percentage increase, but the Atlantic region started off 2 ½ times as big—and got bigger.

The good

The “Atlantic area dominates with 39% of total U.S. gas resources,” the committee noted as it announced the study. Not bad for a region that the industry considered a worked over has-been a little more than a decade ago.

Statistics show Pennsylvania passed Louisiana as the nation’s second-largest gas producer, behind Texas, six years ago. Some industry observers say it’s not far-fetched to project Pennsylvania will be the nation’s top gas-producing state— ahead of Texas—in a few years.

The Pennsylvania Department of Environmental Protection reported the commonwealth’s gas production increased 8.9% from 2016 to 2018, while Texas’ gas output notched upward 0.3%. According to the U.S. Energy Information Administration, Pennsylvania produced more than 18 billion cubic feet per day (Bcf/d) last year, while Texas produced 22 Bcf/d.

Already when taken together, Ohio, Pennsylvania and West Virginia collectively flow more gas than Texas.

Simmons Energy projected in a third-quarter report that Appalachia’s October production would hit a new record, 32.8 Bcf/d. That’s up a healthy 7% from the year-ago month and an increase of 200 MMcf/d from September.

The bad

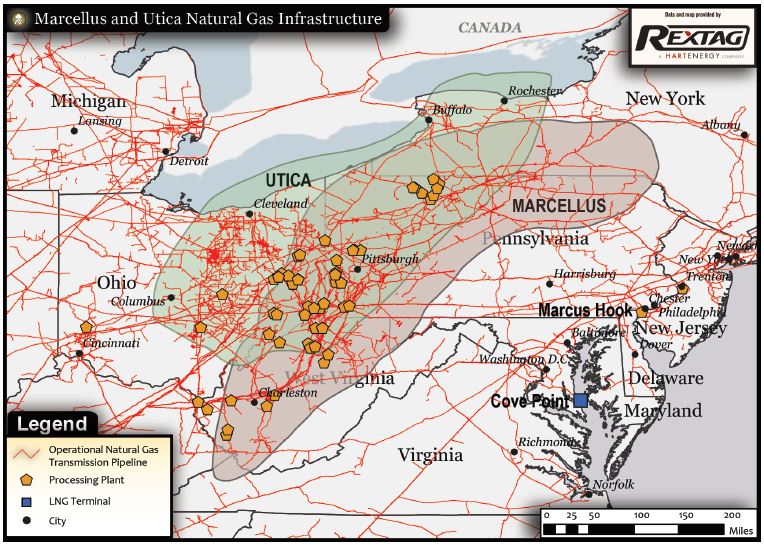

Now for the bad news: How to get that stupendous resource out of the ground and to market? What could Appalachia produce with adequate midstream infrastructure in place to move that gas to the numerous large and nearby markets? You can be sure that will be the primary question on the minds of attendees at Hart Energy’s annual Marcellus Utica Midstream conference in Pittsburgh, scheduled to occur about the time this publication lands in subscribers’ mail boxes.

And what markets they are: New York, Toronto, Detroit, Chicago, Boston and Baltimore/Washington all lie an easy day’s drive away. Dominion Energy’s big Cove Point liquefaction plant on Chesapeake Bay offers easy access to worldwide LNG markets.

The big plays also enjoy direct access to substantial—and growing— petrochemical operations. But even though Pennsylvania gave birth to the oil (and gas) industry as we know it, current residents tend to view the business as a newcomer.

Many fear it.

As one gas producer told Midstream Business about his acreage in Pennsylvania, move in bulldozers, scrape off a hillside and set up a coal mine headframe and area residents don’t say a word. But move in bulldozers, scrape off a hillside and set up a drilling rig “and every phone at the county courthouse starts ringing.” Things have improved in recent years as the plays have matured, but many in the region still regard oil and gas as an outlier, producers and midstream operators say.

That means there’s about as much midstream action currently in courtrooms and legislatures as there is in the field.

Pennsylvania, in particular, struggles with how to regulate the booming industry.

Rule of capture

In September, the commonwealth’s Supreme Court heard oral arguments in a “rule of capture” case that could profoundly impact hydraulic fracturing in the Marcellus and beyond.

At issue in Briggs vs. Southwestern Energy Production Co. is a well fracture that crossed a property line, releasing gas that moved back across the line to be captured at a wellbore in Susquehanna County. The plaintiffs in the case, the Briggs family, maintain that because Southwestern Energy’s fracture extended to the subsurface of their property and allowed the extraction of gas on their property, the company trespassed and the gas extraction was unlawful.

In its defense, Southwestern asserted that it never entered or drilled on the plaintiffs’ property and that the rule of capture—developed from English common law and affirmed by Pennsylvania courts in cases dating to 1889—made the extraction legal.

“The industry in this case takes the position that when you’re hydraulically fracturing rock, you don’t really know where the fractures are going to go,” Harry Weiss, practice leader of the Philadelphia-based Ballard Spahr law firm’s environment and natural resources group, told Midstream Business. “As such, because it’s too difficult to ascertain, the rule of capture should apply so any of the neighbor’s gas you might happen to pull … would be yours—you captured it and you would not owe the neighbor any compensation.”

A trial court granted Southwestern’s motion for summary judgement, agreeing that the rule of capture precluded the request for punitive damages. Then the case went to the Pennsylvania Superior court on appeal, which overturned the trial court and determined that “hydraulic fracturing is distinguishable from conventional methods of oil and gas extraction” and the common law rule of capture did not apply.

In its decision, the court determined that gas in a shale formation is non-migratory by nature, unlike water in aquifers or conventional, porous oil and gas producing zones. It could only have moved from the Briggs property to the adjoining property leased by Southwestern by the application of an external force—hydraulic fracturing. The court also rejected Southwestern’s contention that the difficulty in determining the occurrence of a subsurface trespass and the value of the gas meant that damages cannot be paid.

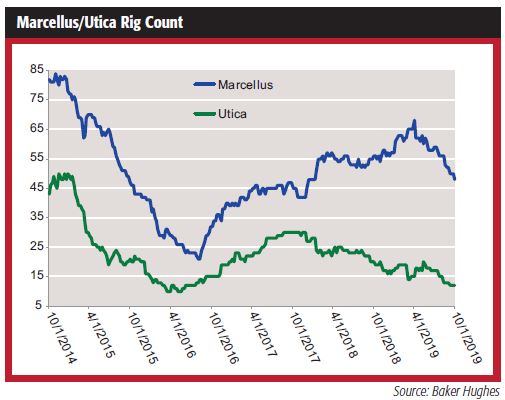

The court likely will decide the case early next year. Meanwhile, the issue places a damper on some producers’ drilling programs. An EnVantage report said the Appalachia plays had 517 drilled but uncompleted (DUC) wells in August. It’s no surprise, then, that the region’s rig count has been dropping.

The ugly

A decision for the plaintiffs could create a blizzard of similar lawsuits in other states. That uncertainty ties into the nation’s interest in renewables and reticence to develop any hydrocarbons, anywhere.

New York State has effectively blocked new pipelines that would serve its residents as well as New England markets. Some industry observers have come to refer to the Empire State’s border with Pennsylvania and New Jersey as the “Wall of Cuomo,” given the continuing, bitter opposition to oil and gas development of any kind by Gov. Mario Cuomo.

The state’s opposition has blocked six gas transmission projects to date.

Opposition exists elsewhere. Work halted on the Atlantic Coast Pipeline, a 600-mile, 42-inch transmission line as the year began. Atlantic Coast, with a planned capacity of 1.5 Bcf/d, would extend from West Virginia to North Carolina. Environmentalists convinced the Fourth Circuit Court of Appeals to vacate a permit issued by the U.S. Fish and Wildlife Service, and now the issue seems headed to the U.S. Supreme Court.

Dominion Energy and its partners, Duke Energy, Piedmont Natural Gas and Southern Co. Gas, remain optimistic that work will resume sometime in mid- 2020. But the delays will prove expensive. Dominion estimated costs will go up by some $1 billion to around $7.5 billion.

Similar legal setbacks have stymied the proposed PennEast Pipeline. A federal appeals court ruled late in the third quarter that the project does not have eminent domain power to seek condemnation of state-owned property in New Jersey. The legal wrangling continues, but industry observers point out that, if upheld, the ruling could throw up a significant development of all pipelines in the U.S.

The 120-mile, 36-inch pipeline would move 1 Bcf/d of gas from western Pennsylvania to New Jersey customers. UGI Energy Services, the midstream unit of local distribution company UGI Corp., leads the project.

Ohio sausage

Next door, Ohio faces its own disagreements. The Clear Energy Alliance recently noted a bill in the Ohio legislature is a “Sausage-O-Rama” that would help solar, nuclear and coal— while it would do nothing to support the state’s booming gas business. The alliance said “HB-6 is a mish-mash of energy legislation. ... These days it seems every government agency is worried about CO2 emissions. So why would this subsidy sausage include coal, but not wind, and decrease future renewable mandates? Politics.”

But as always, the midstream sector finds a way. New midstream infrastructure headed west and southwest has provided the best outlets for Marcellus and Utica production. A recent EnVantage market report noted the major gas transmission systems headed west—Rover, Nexus, REX—have had growing volumes in the last two years.

There are new assets entering service and new customers emerging—some in the region itself—even if the activity has been less than what’s needed, given the scale of the resource.

The Williams Cos., ranked No. 6 on this publication’s Midstream 50 of the sector’s largest public players, has a significant role in Appalachia, given its ownership of the Transco gas transmission system.

Late in the third quarter, the firm placed its Rivervale South to Market project in service. The project expanded the existing Transco system to meet growing heating and power generation demand for consumers in the Northeast.

Rivervale South to Market project provides 190,000 dekatherms of firm gas service by uprating 10.3 miles of existing Transco line, adding less than a mile of new pipeline looping, and upgrading or modifying existing facilities, in New Jersey. Williams noted that’s enough gas to serve 1 million homes.

“The demand for clean, reliable natural gas is at an all-time high, particularly in the northeastern markets where it has had a direct impact on significantly improving regional air quality,” Alan Armstrong, president and CEO, said in announcing the start of service. “The Rivervale South to Market project will continue this progress in a manner that minimizes environmental impacts by enhancing and expanding our existing Transco pipeline infrastructure.”

The Transco system includes approximately 10,000 miles of pipeline, extending nearly 1,800 miles between South Texas and New York City. The system provides the major gas transmission link to 12 southeastern and Atlantic Seaboard states, including major metropolitan areas in New York, New Jersey and Pennsylvania.

One of the region’s biggest players, Marathon Petroleum, continues to add to its strong Appalachian infrastructure position through its MPLX subsidiary, which ranks No. 7 on the Midstream 50. It told investors in a September presentation that its investment in its Northeast gathering and processing operations will still represent some 20% of MPLX’s estimated 2019 EBITDA, even as the firm works to meld in the midstream assets it acquired earlier this year in its acquisition of Andeavor Logistics, formerly Tesoro Logistics.

Petrochemical prize

The big prize for the Appalachian energy industry will be Shell’s world-class Pennsylvania Petrochemicals Complex, going up on the Ohio River in Beaver County, Pa., outside Pittsburgh. When completed, the $6 billion plant will produce 1.6 million tons per year of polyethylene, using abundant Marcellus/ Utica ethane as feedstock.

Shell told Pittsburgh media during a recent press tour that work is on track for completion in 2021, adding that some 6,000 construction workers are at the plant now, and that the plant will create 600 permanent jobs when it goes on stream. All major components of the plant had been installed by the third quarter, a company spokesman said.

It will be the first big cracker built in the U.S. outside the Gulf Coast. Shell touts the location—with adjacent rail, river and Interstate highway access as ideal, centrally located between major U.S. and Canadian markets and close to seaports serving foreign markets.

But the region’s gas-fueled petrochemical industry seems to have taken two steps forward and one step back. Braskem SA announced in the third quarter it would drop a smaller polyethylene cracker proposed for Parkersburg, W. Va. A third cracker, proposed by PTT Global Chemical for a site in Belmont County, Ohio, remains a possibility, although the Thai-based firm has not announced a final investment decision.

NGL plans

Gas produced from the big plays tends to the wet side, providing an abundance of ethane, along with propane, butane and natural gasoline, that could feed that developing petrochemical base. But in the meantime, what to do with it?

Enterprise Products Partners, No. 4 on the Midstream 50, announced in October sufficient shipper interest to move ahead with proposed 50,000 barrels per day (Mb/d) expansion of its ATEX ethane pipeline that moves NGL from the Appalachian Basin to the big gas liquids hub at Mont Belvieu, Texas, outside Houston.

The extra capacity Enterprise has proposed for the 1,200-mile line would come via a combination of pipeline looping, hydraulic improvements, and modifications to existing infrastructure. The expanded capabilities could be in service by 2022, Enterprise said.

Another big NGL expansion project, Energy Transfer’s proposed Mariner East 2, linking western Pennsylvania and Marcus Hook, outside Philadelphia, is tied up in controversy. The original Mariner East line, completed in 2015, feeds liquefied ethane exports to European petrochemical plants.

Dallas-based Energy Transfer ranks No. 2 on the Midstream 50.

Wall Street woes

All this doesn’t help, given the investment community’s current cold shoulder to all of the energy industry.

“U.S. energy markets are coming to the end of their latest infrastructure cycle just as the reality of tight capital markets is sinking in,” Rusty Braziel, president, CEO and principal consultant for RBN Energy. He added, “…there is a chill in the air. … Easy access to capital is a thing of the past,” in a recent report.

That reticence shows up in midstream capital planning, of course. Gary Heminger, chairman and CEO of MPLX LP, talked about his firm’s plans in his second-quarter earnings call.

“First, we expect to streamline our capital expenditures, focusing on the most attractive returns,” Heminger said. “Second, we are working with [parent Marathon Petroleum Corp.] MPC on a portfolio optimization initiative, which could include potential asset divestitures. Third, we plan to use the proceeds from any divestitures for general purposes such as investments and high-return projects, as well as debt reduction.

“We believe these initiatives will help MPLX continue to be one of the best-positioned midstream platforms in the industry for long-term value creation,” he added.

MPLX ranks No. 7 on the Midstream 50. It has significant gathering, processing and transportation operations in the Marcellus and Utica. But it also recently acquired Andeavor Logistics (formerly Tesoro Logistics) with significant—and potentially easier to develop—operations in the Permian Basin and Bakken Shale. Capital likely will flow to those plays instead.

Arabs and Appalachia

But things could be looking up for Appalachian infrastructure in the wake of the attacks on Saudi Arabian assets in September. Tom Gellrich, founder of Philadelphia-based Topline Analytics, said in a recent statement the attacks make assets in the politically stable U.S. much more attractive.

“The Saudi attacks, unanticipated with military precision, against highly defended targets adds an untenable risk premium to any Middle East investment,” Gellrich said. “After decades of relatively stable and consistent strategies the Western petrochemical majors are changing at an unprecedented pace. … These attacks make the Appalachian Basin an even more viable region for the petrochemical industry” and the related midstream assets that support it.

Wells Fargo Securities noted the impact of the energy business in general, and the midstream in particular, in a recent special report that noted the state’s mining, oil and gas sector enjoyed 18.4% growth, year over year, in first-half 2019.

An “abundance of natural gas supports a wide array of jobs in the state, many of which go beyond the exploration, extraction and refining industries, extending to other sectors, such as construction, manufacturing, engineering and other professional support services,” Wells Fargo said.

“Increased natural gas production has brought with it the need for a more robust energy infrastructure and has led to a surge in heavy and civil engineering construction jobs over the past few years. The pace of employment growth, however, has eased a bit more recently. Pennsylvania still has thousands of miles of natural gas pipelines under construction, second only to Texas. The Mariner East 2 pipeline, which will carry natural gas liquids from western Pennsylvania to a processing and export facility near Philadelphia, has faced some delays recently but is a shining example of the ongoing energy infrastructure buildout.”

____________________________________________________________________________________________________________________________________

[SIDEBAR STORY]

Fueling Growth At Home And Around The World

In recent weeks, Pennsylvania’s Department of Community and Economic Development acted on an invitation from Australia’s Northern Territory to visit and share our state’s experience with the development and application of natural gas. I was honored to accompany the commonwealth’s representatives on behalf of Pennsylvania’s manufacturing sector, which relies on affordable, available and reliable energy and whose success depends on wise energy policy decisions from Harrisburg.

What we learned Down Under illuminates our energy management choices in Pennsylvania: Even as the Northern Territory is working on how best to develop the natural gas opportunity in the Beetaloo Basin, Australia in general has overcommitted to LNG exports, an unintended consequence of which has been to stifle Australia’s manufacturers with high energy prices and shortages of domestic supply.

Back home, Forbes reports that 2019 is set to be the biggest year yet for the emerging U.S. natural gas export business, and America is expected to surpass Malaysia to become the world’s third-largest LNG exporter.

In our region’s Marcellus play, there is often debate about gas exports and whether we are at risk of exporting too much, at the expense of economic growth in Pennsylvania. Or, put another way, if too much of our gas leaves Pennsylvania, will we miss the opportunities to add value to the resource locally, which grows jobs, businesses, and strengthens communities?

Fortunately, the gas reserves in the Marcellus and Utica plays should allow us to optimize use in the Pennsylvania-Ohio-West Virginia region even as we continue to sell for export. And beyond development of the gas, the presence of such significant energy assets should position us as a prime location for the next generation of advanced manufacturing— including the design and production of advanced materials. This will help increase employment (and drive population growth), and reap what is estimated to be tens of billions in expanded GDP.

NGLs

In addition to the gas that powers and heats our businesses and homes, NGLs are produced here. NGLs are a key component for making plastics, resins, fuels and chemicals that are fundamental to countless products we rely on every day.

The “Forge the Future Phase 1” econometric study report showed that Pennsylvania’s vast amounts of gas and NGLs are meeting relatively weak demand growth in-state, and limited, but growing, pipeline capacity to move it. As a result, Pennsylvania’s voluminous gas supply is currently being sold at a steep discount, which makes it attractive for export. The report also found that because of our abundant supply, those exports are unlikely to raise prices here to a level that would impair our manufacturing cost competitiveness or hurt consumers.

Establishing export markets has spurred the production that is now coming online for greater domestic use. If we pivot now to the Forge the Future report’s agenda for an energy-enabled economy, Pennsylvania can benefit—immensely—from both.

There are foundational elements to the pursuit of a new, automated and data-driven manufacturing era for Pennsylvania, supported by the significant energy reserves in our region. Let’s:

- Benefit a broad base of Pennsylvanians with more jobs, better jobs and greater job stability. Work in gas development and downstream advanced manufacturing delivers family-sustaining wages that will return minimum-wage jobs to what they used to be: a place to start, learn and grow, not a destination.

- Ensure that there is enough gas demand growth—in-state and for export—to make gas production economical. Natural gas producers in many cases currently make little or no profit in the region—they are investing for the long run.

- Work together to apply existing technologies and develop new ones that bring our economic, environmental and health interests into alignment.

A range of efforts are underway to help Pennsylvania fulfill its potential. Pennsylvania joined Ohio and West Virginia again as a member of the Tri-State Shale Coalition to collaborate on strategic ways to build our energy- and manufacturing-driven economy. Pennsylvania Gov. Tom Wolf has also recently created the Governor’s Office of Energy to lead and coordinate growth strategies and tactics across the Commonwealth. Additionally, Pennsylvania House Speaker Mike Turzai and other House Republicans rolled out a package of bills called Energize PA, which is intended to expand the manufacturing potential of the shale boom.

Plans for a regional storage and trading hub for natural gas and NGLs are advancing. The state’s pipeline network—which provides a range of benefits compared to surface transport over highways and rail— is growing and our affordable energy is reaching more residents.

Based on Forge the Future data, successful development of downstream industries holds the potential for significant economic growth in Pennsylvania: a $60 billion increase in Pennsylvania GDP, the addition of more than 100,000 jobs and an increase in natural gas demand of 4-5 trillion cubic feet. Collectively, this could generate several billion dollars in additional tax revenue for the commonwealth and help us grow our way to sustained fiscal health, and a better quality of life.

David N. Taylor is president and CEO of the Pennsylvania Manufacturers’ Association.

Recommended Reading

Range Resources Holds Production Steady in 1Q 2024

2024-04-24 - NGLs are providing a boost for Range Resources as the company waits for natural gas demand to rebound.

Hess Midstream Increases Class A Distribution

2024-04-24 - Hess Midstream has increased its quarterly distribution per Class A share by approximately 45% since the first quarter of 2021.

Baker Hughes Awarded Saudi Pipeline Technology Contract

2024-04-23 - Baker Hughes will supply centrifugal compressors for Saudi Arabia’s new pipeline system, which aims to increase gas distribution across the kingdom and reduce carbon emissions

PrairieSky Adds $6.4MM in Mannville Royalty Interests, Reduces Debt

2024-04-23 - PrairieSky Royalty said the acquisition was funded with excess earnings from the CA$83 million (US$60.75 million) generated from operations.

Equitrans Midstream Announces Quarterly Dividends

2024-04-23 - Equitrans' dividends will be paid on May 15 to all applicable ETRN shareholders of record at the close of business on May 7.