Breakeven costs have fallen for deepwater projects, but analysts question whether the oil industry is ready for anticipated cost inflation. (Source: Shutterstock.com)

Oil and gas companies with the stamina needed to dive into deepwater projects and stay afloat have managed to slash breakeven costs in recent years. But analysts warn impending cyclical cost inflation could trigger a rise in such costs.

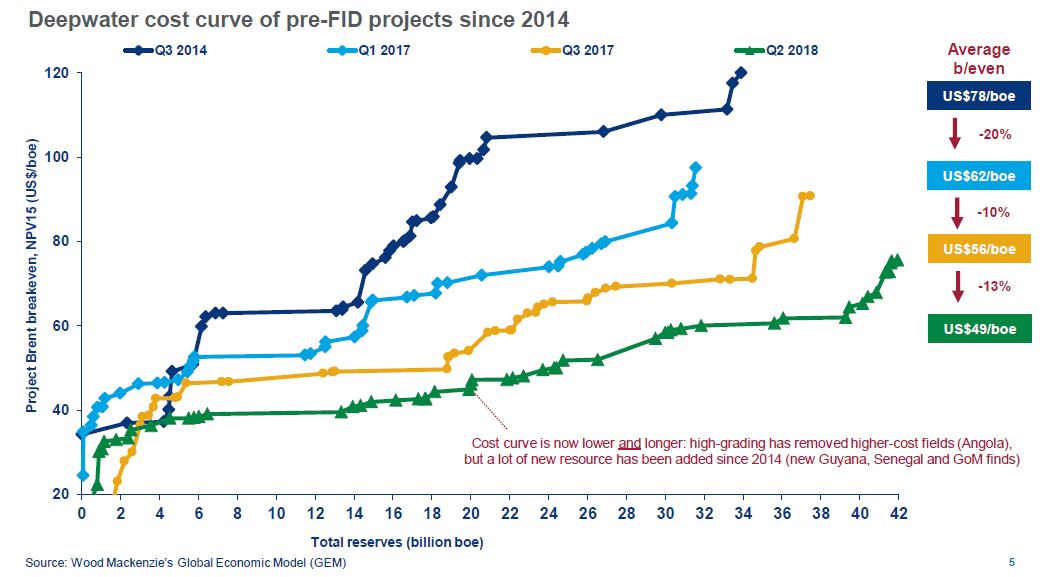

The average pre-final investment decision breakeven dropped to US$49 per barrel of oil equivalent (boe) today compared to $78/boe in 2014, according to a report released Nov. 27 by Wood Mackenzie. Carrying out lessons learned during the most recent market downturn, some operators have opted for fewer wells, more phases and tiebacks to existing infrastructure while seeking lower rig rates and supply chain costs, drilling better wells and utilizing technology to control expenses.

BP, for example, cut costs for the Mad Dog Phase 2 project in the deepwater U.S. Gulf of Mexico (GoM) by more than half. Focusing on value, industry solutions and collaboration with its partners BHP and Chevron USA Inc. affiliate Union Oil Co. of California, the operator chopped the massive 33-well $20 billion development down to $9 billion with up to 14 wells.

RELATED: BP Gives Mad Dog 2 Floating Production Unit New Name

The project, which is set to begin oil production in late 2021, remains on budget and on schedule, Starlee Sykes, BP’s regional president for the Gulf of Mexico and Canada, said in a news release.

“This project is key to delivering high-margin production from one of the largest fields in the Gulf of Mexico, and it will strengthen our position in the basin for years to come,” Sykes said.

Similar stories have unfolded across deepwater GoM, where the number of subsea tiebacks has grown, and other parts of the world. Unit costs have fallen by more than 50% since 2013, said Wood Mackenzie. The firm added that improved project execution has resulted in the average deepwater project sanctioned between 2014 and 2016 starting up about 5% under budget, compared to the 10% to 15% overrun typically seen with projects between 2006 and 2013.

Improved project economics means more deepwater investments could be on the horizon, following the market downturn that halted or slowed many offshore projects. Wood Mackenzie forecasts developments offshore Guyana, Brazil and Mozambique will drive higher deepwater capex, expected to hit nearly $60 billion by 2022 from about $50 billion today.

But the costs gains could be short-lived if companies fail to make the savings permanent.

“The return of cyclical inflation could see this epic period of deepwater cost reduction come to a close,” said Angus Rodger, research director for the Wood Mackenzie.

Cyclical inflation could impact deepwater costs in the areas of rig day rates, subsea equipment and services and other service sector costs, according to Wood Mackenzie. The speed of cyclical cost re-inflation will depend on how quickly operators drive a recovery and the supply chain’s ability to meet their demand, the firm said in the report.

“The question now is how much of the ‘structural’ cost savings we have seen through the downturn will prove sustainable through the investment cycle, and which are just short-term company adaptions,” Rodger added.

Structural costs savings, considered more “resilient/sticky” by Wood Mackenzie, include drilling faster and better wells, having quicker project lead times and phasing projects. The firm said that it was skeptical that some of these so-called “structural cost savings will stand the test of time in a sustained cyclical uptick.” Such savings were viewed by the analysts as external environment-driven corporate behavior and project design changes.

“Those that ‘stick’ become cultural changes within the sector that can stand the test of time and price cycles, but historically the big players in deepwater have been slow to change, based on their size, culture and limited risk tolerance in a challenging operating environment,” the report said.

Velda Addison can be reached at vaddison@hartenergy.com.

Recommended Reading

Petrobras to Step Up Exploration with $7.5B in Capex, CEO Says

2024-03-26 - Petrobras CEO Jean Paul Prates said the company is considering exploration opportunities from the Equatorial margin of South America to West Africa.

After 4Q Struggles, Transocean’s Upcycle Prediction Looks to Pay Off

2024-02-21 - As Transocean executives predicted during third-quarter earnings, the company is in the middle of an upcycle, with day rates and revenues reaching new heights.

Oceaneering Won $200MM in Manufactured Products Contracts in Q4 2023

2024-02-05 - The revenues from Oceaneering International’s manufactured products contracts range in value from less than $10 million to greater than $100 million.

E&P Highlights: Feb. 5, 2024

2024-02-05 - Here’s a roundup of the latest E&P headlines, including an update on Enauta’s Atlanta Phase 1 project.

CNOOC’s Suizhong 36-1/Luda 5-2 Starts Production Offshore China

2024-02-05 - CNOOC plans 118 development wells in the shallow water project in the Bohai Sea — the largest secondary development and adjustment project offshore China.