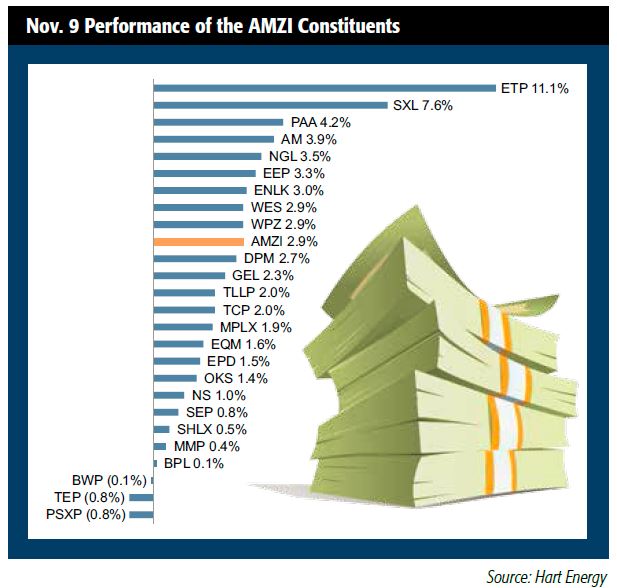

One could argue, President-elect Trump has already added value to midstream MLPs: on Nov. 9, the day after the election, the Alerian MLP Infrastructure Index (AMZI) rose 2.9%. Energy Transfer Partners (ETP), which is building the controversial Dakota Access Pipeline, rose 11.1%. As a result of major media attention, ETP is now a leading example for investors of how MLPs can benefit from reduced regulatory risk.

One focus of President-elect Trump’s political campaign has been “vital energy infrastructure projects.” Midstream MLPs play a critical role in building, maintaining and operating these assets. Here’s how his proposed policies could impact the sector:

Reduced permitting regulations could get steel into the ground more quickly, as his invitation to TransCanada to reapply for a permit to build the Keystone XL Pipeline implies. However, getting government out of the way of business leaves eminent domain conflicts unresolved. It is unclear whether an individual landowner would be able to force an MLP to reroute a pipeline, or whether the necessity of infrastructure outweighs the rights of the individual landowner.

Trump’s focus on regulations that benefit the American worker mean that safety and maintenance regulations would likely remain in place. If handled sensibly and correctly, regulations, like law and order, benefit everyone. By avoiding environmental disasters and keeping our workers safe, midstream MLPs can focus on the real, profitable business of processing, transporting and storing our nation’s energy.

Opening federal lands to natural resource extraction to create jobs has also been a key campaign point. However, for U.S. oil and gas companies, the limiting factor is not available reserves but the low cost of commodities. Many wells on known private land remain uneconomic. While coal MLPs have seen their unit prices rise, any measures taken that would improve the economics for oil and gas companies would only increase the competition for coal (and vice versa).

Taxing all partnerships at corporate levels would remove a significant MLP investment incentive. MLPs benefit from pass-through status and consequently, frequently pay higher yields than corporations. That said, the 2015 JCT tax expenditure study indicates that publicly traded partnerships engaged in energy-related activities are estimated to cost the government around $1.2 billion per year in foregone revenue, limiting the downside impact.

Lower corporate and individual tax rates, in the absence of changing partnership taxation mentioned above, could still change the makeup of the asset class. Again, as pass-through entities, MLPs would not directly benefit from a lowered federal corporate tax rate. Instead, those MLPs already looking at abandoning the structure in favor of becoming C corporations—a trend that began with the Kinder Morgan reincorporation in 2014—may be further encouraged to do so. For those MLPs that remain partnerships, a lower individual tax rate could reduce the value of the tax deferral associated with MLP distributions.

Maria Halmo is the director of research at Alerian, an independent provider of MLP and energy infrastructure market intelligence. Over $15 billion is directly tied to the Alerian Index Series. For additional commentary and research, visit www.alerian.com/alerian-insights.

Recommended Reading

BOEM Announces Next Steps for GoM Lease Sales 262, 263, 264

2024-04-01 - BOEM said Lease Sale 262 is expected to take place in 2025.

US Proposes Second GoM Wind Lease Auction

2024-03-20 - Combined, the four proposed areas for offshore wind have the potential to power about 1.2 million homes if developed, according to the Interior Department.

DXP Enterprises Buys Water Service Company Kappe Associates

2024-02-06 - DXP Enterprise’s purchase of Kappe, a water and wastewater company, adds scale to DXP’s national water management profile.

ARM Energy Sells Minority Stake in Natgas Marketer to Tokyo Gas

2024-02-06 - Tokyo Gas America Ltd. purchased a stake in the new firm, ARM Energy Trading LLC, one of the largest private physical gas marketers in North America.

California Resources Corp., Aera Energy to Combine in $2.1B Merger

2024-02-07 - The announced combination between California Resources and Aera Energy comes one year after Exxon and Shell closed the sale of Aera to a German asset manager for $4 billion.