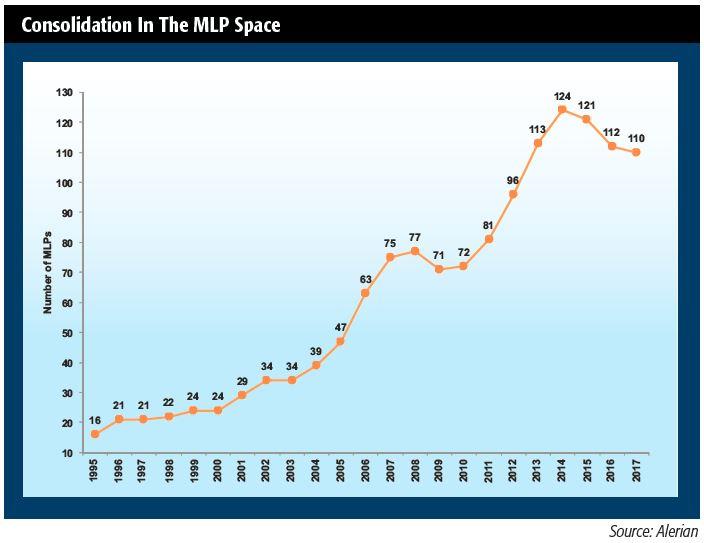

At the end of 2014, there were a record 124 MLPs trading. By the end of 2015, that number had fallen to 121, and by the end of 2016 there were only 112. At the end of January 2017, there were 110 and, if all pending mergers are approved, another handful will disappear. The loss of over a dozen companies has begun to worry some investors.

While MLPs are generally insulated from moderate moves in commodity prices, the huge fall in the price of crude oil, combined with minimal recovery, has impacted the more commodity-sensitive MLPs. Many upstream MLPs declared bankruptcy over the past two years and are no longer trading on major exchanges.

Midstream MLPs may be more insulated from commodity price moves but they are not immune. As their customers struggled, and some contracts were not renewed, the fundamentals of midstream MLPs suffered. Negative investor sentiment across the entire energy sector further depressed prices, increasing the cost of equity for MLPs. As leverage ratios rose, so too did the cost of debt.

In order to lower their cost of capital so they could continue to pursue growth, many MLPs bought out a parent’s incentive distribution rights or merged with each other or a parent company. While the bankruptcies of the commodity-sensitive MLPs are indeed worrying, smarter combinations and capital structures will remove growth headwinds.

As MLPs continue to position themselves to pursue growth, 2017 is likely to see more merger and simplification announcements. The space may begin to barbell into a handful of mega-caps and many small- or micro-caps with the result that the largest companies will need to both compete for bids and cooperate when joint ventures are necessary. The smaller midstream companies must find and defend their niches and unique offerings.

With few MLP S-1s filed with the U.S. Securities and Exchange Commission, indicating plans to go public and create new companies, each company that remains trading can spend the next few years building its individual moat without competition from new entrants.

Consolidation is a natural part of many industries, particularly those which require significant upfront infrastructure investment. As such, the absolute number of MLPs should not be investors’ primary focus when considering the future of the space. More than whether a company is structured as a C corporation or an MLP, its existing footprints, cost of capital and availability of labor will determine how well it is positioned to participate in the buildout of North American energy infrastructure over the next several decades.

Maria Halmo is the director of research at Alerian, an independent provider of MLP and energy infrastructure market intelligence. Over $17 billion is directly tied to the Alerian Index Series. For additional commentary and research, please visit www.alerian.com/alerian-insights.

Recommended Reading

Matador Stock Offering to Pay for New Permian A&D—Analyst

2024-03-26 - Matador Resources is offering more than 5 million shares of stock for proceeds of $347 million to pay for newly disclosed transactions in Texas and New Mexico.

From Restructuring to Reinvention, Weatherford Upbeat on Upcycle

2024-02-11 - Weatherford CEO Girish Saligram charts course for growth as the company looks to enter the third year of what appears to be a long upcycle.

NOV's AI, Edge Offerings Find Traction—Despite Crowded Field

2024-02-02 - NOV’s CEO Clay Williams is bullish on the company’s digital future, highlighting value-driven adoption of tech by customers.

Hess Corp. Boosts Bakken Output, Drilling Ahead of Chevron Merger

2024-01-31 - Hess Corp. increased its drilling activity and output from the Bakken play of North Dakota during the fourth quarter, the E&P reported in its latest earnings.

The OGInterview: Petrie Partners a Big Deal Among Investment Banks

2024-02-01 - In this OGInterview, Hart Energy's Chris Mathews sat down with Petrie Partners—perhaps not the biggest or flashiest investment bank around, but after over two decades, the firm has been around the block more than most.