(Source: Hart Energy)

[Editor's note: A version of this story appears in the August 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

The E&P mantra of living within cash flow leaves investment bankers with few tools on the table to be creative. Equity issuance is largely taboo, with E&Ps generally discouraged from even testing the public market. Refinancing existing debt is likely feasible for higher-quality issuers, but may be a precarious procedure for smaller E&Ps, since debt has come to be viewed as a four-letter word.

Of course, there are exceptions to the rule. The first half of this year has seen a follow-on offering and an IPO in the minerals sector, and more such offerings are said to be in the works over the balance of the year. Likewise, there have been equity issues in the midstream sector, including Diamondback Energy Inc. spinning off an IPO in the form of Rattler Midstream LP.

But perhaps most impactful, according to some industry observers, would be an outbreak of “mergers of equals.” This would likely be sparked by growing recognition of the need for scale to achieve a lower cost of capital and greater efficiencies in operations. Synergies in general and administrative (G&A) expenses would also be a key driver of such mergers of equals.

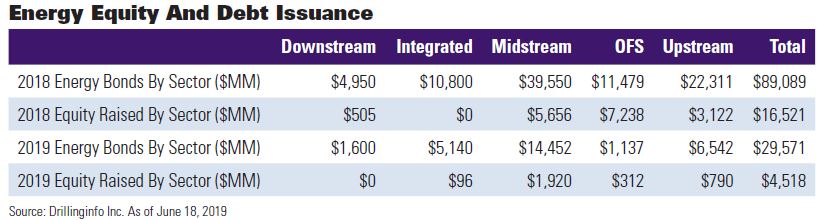

Across the board, revenues in energy investment banking are down markedly, as year-to-date equity and debt issuance have trailed prior-year levels by a wide margin. Looking back another year, revenues are running at barely half the 2017 run-rate, said one investment banker.

‘Dearth’ of Offerings

“There’s a significant reduction, or dearth, in capital market offerings now,” commented Tim Perry, global co-head of oil and gas investment banking with Credit Suisse. With shareholder pressure on E&Ps to adopt a returns-oriented strategy, focusing on free cash flow over growth, “by definition, you’re not outspending cash flow,” he said. “And, in turn, you don’t need to go to the capital markets to fund your growth.”

In addition, the sector has “largely de-levered itself,” according to Perry. “I think the sector generally feels comfortable that their leverage statistics are fine, so they don’t need to repair their balance sheets. And, again, they don’t typically need to go to the equity capital markets to fund their capex needs because those needs are being met now from internally generated funds.”

Various factors have made the industry less attractive to investment banking. The energy weighting in the S&P 500 Index has continued to slide to around 5%. In addition, the sector has suffered from bouts of commodity volatility, notably late last year and in late-May/early June of this year. West Texas Intermediate slumped to about $45 per barrel (bbl) in late December and, after recovering, retreated from $60-plus to the low $50s in early June.

“The industry is facing a lot of challenges in getting investor interest in the sector right now,” said Perry.

Capital markets activity got off to a particularly weak start this year. According to Christopher George, director of Drillinginfo Inc.’s Capitalize database, the first quarter saw “the fewest equity deals this decade.”

Nonetheless, Credit Suisse has managed to win its share of business from the fairly modest number of equity issues raised of late in the energy sector. But it’s been no easy task, said Perry.

“It’s tough out there,” he emphasized. Given the backdrop, “we’re doing okay,” he added. “And okay is pretty good for right now.”

Minerals and Midstream

Notably, in minerals, Credit Suisse was the lead left bookrunner for the IPO of Brigham Minerals Inc., an issue that was upsized from initially 13.5- to 14.5 million shares, and then expanded further with full exercise of the overallotment for a total deal size of 16.675 million shares. The Brigham offering was priced at the high end of the initial offering range of $15 to $18 per share.

Credit Suisse similarly served as lead left bookrunner for the IPO of Rattler Midstream LP, a spin-off of the midstream assets of Diamondback Energy Inc. The offering was expanded from initially 33.3- to 38 million shares, with the 15% overallotment option exercised in full for a total deal size of 43.7 million shares. The IPO was priced at $17.50 per share, the midpoint of the initial offering range.

A follow-on offering in the minerals sector was completed earlier in the year by Viper Energy Partners LP. Viper, also a subsidiary of Diamondback was similarly spun off in an IPO last year. Credit Suisse was sole lead bookrunner for this year’s offering, which was raised from 8- to 9.5 million shares. From filing to offering, the deal was priced at a 5.4% discount.

“One area of capital markets where we continue to find investor interest is in minerals. There’s a lot of positive energy in that group right now,” observed Perry. “The Brigham Minerals offering was more than six times oversubscribed. Investors want free cash flow. And, of course, without the burden of capex, the mineral companies do produce a lot of free cash flow.”

Perry also raised the prospect of transactions by private-equity-backed companies that own minerals. “I think that there is going to be more consolidation in that group,” he said. “Several companies are thinking about merging with other companies in the sector to gain scale. And some mineral companies are considering whether to go public.”

On the midstream side, Perry described Rattler as a “unique deal in the market,” primarily due to its position in providing midstream services to Diamondback. “Diamondback has an incredible track record of value creation for its stockholders,” he said. The offering was heavily oversubscribed, “and obviously it’s traded very well in the aftermarket.”

How does the pipeline for equity issuance look over the balance of the year?

“I think you’ll expect to see across energy a limited supply of transactions. I think you’ll find maybe one or two potential transactions in midstream, and you’ll have one or two transactions in minerals,” said Perry. “I think the transactions you’ll see will have free cash flow through the cycle.”

Mergers of Equals

For Steve Trauber, head of global energy investment banking at Citi, M&A activity looms large for the energy sector as a means to attract interest from the investment community. In particular, to remain relevant, mergers of equals are likely to accelerate with a focus on companies whose enterprise value (market cap plus net debt) is $5 billion or less, he said.

“The biggest thing going on now in the sector is M&A consolidation in the upstream space,” said Trauber. “All the companies are seeking to gain scale. Companies with an enterprise value of $5 billion or less know that they’re undersized, that they don’t have enough scale, don’t have enough efficiencies, and the balance sheets are probably not as big as they need them to be.

“A growing number of small-cap companies are finding it increasingly hard to attract energy equity investors,” Trauber continued. “It’s going to be a game of scale and driving down costs. It’s a commodity business, at the end of the day. You’ve got to have a low cost of capital, you need to have great efficiencies and you need to have some clout over your suppliers, and so on.”

Speaking with Investor in early June, the Citi banker predicted multiple mergers occurring in the balance of the year.

“I think you’re going to see at least five to 10 M&A deals in the next six months,” he said. “There’s a lot of dialogue going on under the surface. A lot of them are going to end up effectively being mergers of equals. That doesn’t mean you won’t have one company sort of survive; in certain cases it may be more of an acquisition.”

No More Premium Takeouts

Potential transactions “are going to have the feel of a merger as opposed to a big premium takeout, because nobody can afford big premiums to their stock price,” said Trauber. “These E&Ps tend to trade at around the same multiple, so the benefits of this are really gaining scale and efficiencies, cutting G&A expense and taking out some field costs to make a company investible again.”

In terms of potential synergies, G&A expenses are clearly a key factor, and post-merger you obviously “don’t need two CEOs, two CFOs, etc.,” noted Trauber. “If you’re in the same basin, you’ve got field costs. You still need people, but there’s some overlap there, for example.” Based on prior transactions, “you end up finding more synergies than you think are out there,” he added.

The Permian, not surprisingly, is the basin considered most fertile for mergers, according to Trauber.

“The big guys want to buy oil, and the biggest, cheapest resource that exists is in the Permian,” he said. “So you can imagine that everyone wants to be buying in the Permian. There are only a few large, low-cost resource bases in the world. You’ve got Saudi Arabia, Russia, Brazil and maybe the Gulf of Mexico, and then you’ve got the Permian, which seems to be easiest and most accessible.

“I think you’re going to continue to see companies merge there to get bigger and become attractive to some of the majors,” said Trauber, noting Chevron Corp. remains a likely buyer after its unsuccessful bid for Anadarko Petroleum Corp .

“I do believe that major oil companies are going to make acquisitions of size in the Permian. They need more resource. The question is: When and whom?”

Chevron: Stay ‘Disciplined’

“Chevron has expressed an interest to be bigger in the Permian. There’s no surprise around that,” Trauber continued. “They’ve also expressed a strong opinion about being disciplined about how they do it and not overpaying to meet their objective. I think there are numerous opportunities in the Permian for them to continue to grow their business through acquisitions.”

In terms of timing for a potential acquisition, “I would be very surprised if you don’t see them do that over the course of the next 12 to 24 months,” he said. “Do I expect them to do it in the next six months? Probably not, but I think they’ve got a very strong balance sheet, they’ve got good cash flow and they have a strong desire to be bigger in the Permian. So I do think they will be a buyer.”

As regards smaller players in the Permian waiting for better conditions, Trauber struck a note of caution.

“No CEO wants to sell his stock when you’re off 30% in the last 12 months or so,” he observed. “You hope to sell at a strong valuation, and these are relatively weak valuations. My view is that you go ahead in spite of that now, or risk facing a continuing deterioration of valuation. As the valuation gets weaker on a relative basis, it’s going to be harder to use its currency to help de-lever.”

However, assuming key criteria are met—such as rock quality, strength of balance sheet and appropriate synergies—E&Ps may ultimately be able to “get comfortable with stock-for-stock deals,” he said. “That’s where you’re really merging, you’re not selling and you take the stock of a stronger, more liquid company with an enhanced balance sheet. That’s the way people have to look at it.”

Elsewhere, Trauber described the market for energy IPOs as “extraordinarily cold.” One exception, he said, is the mineral sector, where various private-equity sponsors may combine mineral interests held by portfolio companies in preparation for going public. Alternatively, these interests may be merged into an existing, more liquid public mineral company in exchange for a mix of stock and cash.

Another exception may be the oilfield equipment sector. An example is, Houston-based wellhead manufacturer Cactus Inc., which is characterized by “highly differentiated, high-margin, strong free-cash-flowing oilfield equipment,” according to Trauber. The company has “market leadership, low capex and generates high rates of return on capital employed.”

The SPAC Struggle

As for raising money via a special purpose acquisition company, or SPAC, said Trauber, “they’re just another form of going public. You can probably raise money in a SPAC, but then you have to find an acquisition target and bring energy investors into it, much like with an IPO. What will happen is that the SPAC investors will trade out, and you’ve got to establish a new following with energy investors. If you can’t do an IPO, you’ll really struggle to do a SPAC.”

Recent conditions in investment banking “are some of the toughest I’ve seen in my 20 years on the capital markets front,” said Nathan Craig, managing director with J.P. Morgan Chase & Co. Among the factors he cited for the slump: A lack of issuance in capital markets, clients being “inwardly focused” and “shareholder frustration.”

“Broadly speaking, clients have got the message that everyone’s meant to be self-funding,” said Craig. “Even if the capital markets were open at a price, you’re not meant to be using them. There’s the risk of a stigma if you were to run out and issue equity. The A&D market has been dismal, as well, and the reason for that is that the funding market has been challenged.”

Debt Now A ‘Four-Letter Word’

As regards the high-yield market, “for a lot of people, debt has now become a four-letter word,” he continued. “If it’s not a refinancing of existing paper, clients have been reluctant to add incremental debt to the balance sheet. So issuance in credit has gone down, with the year-to-date level through May running at about one-quarter of prior-year levels.”

The exception to the above is again minerals, which offers “a bright spot of activity,” according to Craig.

“We expect two or three mineral IPOs in the next 12 months. There is some concern by investors that if you have too many mineral IPOs, then you get too much fragmentation, like we have in the E&P space currently. But minerals are hitting all the check marks investors want: free cash flow, modest growth, sustained dividend, low leverage and a real return on equity.

“There is absolutely a home for minerals. If you consider the market capitalization of public mineral companies compared to the opportunity represented by the entire mineral sector, public mineral companies represent only around 2% of the total value that is out there,” he estimated. “There just aren’t a lot of mineral opportunities in the public-equity domain today.”

J.P. Morgan served as active bookrunner of the Rattler offering, which Craig described as being “substantially oversubscribed with incredibly high-quality names.” Investors making money in Rattler may help open the energy IPO market, he said, but other offerings may not be quite as competitive.

“It’s a little bit more of a challenge to bring a true new issue to the market with an unknown asset base, unknown management team, unknown track record. That’s not to be underestimated,” he cautioned. “The first thing institutional investors will ask is: ‘Why do I need to own this? Tell me why I can’t get similar exposure to this through someone else in the marketplace?’

“A governor of the IPO market from institutional investors—mainly upstream, but also midstream—is, ‘Why do I need to own a forthcoming IPO when I can buy another great name company for an extremely low multiple over here?’ It’s also, ‘How does it compete with all the other things I can buy that are trading very cheaply?’ That makes IPOs hard right now.”

Shareholder And Management Frustration

In terms of market sentiment, “there is frustration among shareholders and managements,” observed Craig, while banking clients “are inwardly focused right now.” For example, with some onshore E&Ps trading at or around PV10 values, questions arise: ‘Why aren’t you rewarded for what you’re doing in your core operations?’ No matter what you do operationally, it’s not translating into your valuation multiples.”

On the issue of G&A expenses, Craig said “it’s hard to underestimate the amount of attention that investors are focusing on G&A. And that is a function of the frustration that they feel and the lack of investment returns. You have shareholders frustrated, and you have boards and management teams frustrated.”

As regards M&A, “more than ever before there seems to be a belief—and this is coming from E&P clients—that there’s a minimum market cap that you need to have in order to garner investor attention. Even if you’re at that level, gaining investor attention can still be extremely challenging. And if you are not at that level, it makes the hurdle even higher for relevance,” Craig said.

Commodity Volatility

An added hurdle to overcome has been recent commodity volatility, which hasn’t helped as the energy sector “transitions toward trying to meet what are relatively new metrics, such as living within cash flow, lowering leverage, etc.,” noted Craig. “This kind of pivot is not something that happens overnight. And if you get significant volatility, it’s just unhelpful for investors.”

As the E&P sector moves forward to meet these goals, the task ahead for the upstream players is to “drive efficiencies so that they can deliver to the shareholder a return commensurate with the risk profile and the underlying commodity volatility in this industry,” he advised. “And until you can demonstrate that, the shareholders are largely on strike.”

In a market where capital options are few and far between, are there any avenues in energy to explore?

From high yield’s collapse last December—ending the month without a single deal for the first time since 2008—the sector has improved somewhat, although volatility of late is “undermining” the recovery, according to Craig. Year-to-date energy issuance came to about $2.5 billion from five issues through May, down 75% from $10.2 billion from 24 deals in the year-earlier period, he said.

Drillcos are worth exploring, especially “in an era in which net asset value isn’t being rewarded,” said Craig. If E&Ps have to hold acreage and have a good line of sight on the economics of wells drilled on “good acreage with very solid rock, then I can see why E&Ps execute plans with Drillcos. In this capital-constrained market, I absolutely understand why there are increased conversations occurring around Drillcos.”

Chris Sheehan can be reached at csheehan@hartenergy.com.

Recommended Reading

The OGInterview: Petrie Partners a Big Deal Among Investment Banks

2024-02-01 - In this OGInterview, Hart Energy's Chris Mathews sat down with Petrie Partners—perhaps not the biggest or flashiest investment bank around, but after over two decades, the firm has been around the block more than most.

Kissler: OPEC+ Likely to Buoy Crude Prices—At Least Somewhat

2024-03-18 - By keeping its voluntary production cuts, OPEC+ is sending a clear signal that oil prices need to be sustainable for both producers and consumers.

Buffett: ‘No Interest’ in Occidental Takeover, Praises 'Hallelujah!' Shale

2024-02-27 - Berkshire Hathaway’s Warren Buffett added that the U.S. electric power situation is “ominous.”

The One Where EOG’s Stock Tanked

2024-02-23 - A rare earnings miss pushed the wildcatter’s stock down as much as 6%, while larger and smaller peers’ share prices were mostly unchanged. One analyst asked if EOG is like Narcissus.

Chesapeake Slashing Drilling Activity, Output Amid Low NatGas Prices

2024-02-20 - With natural gas markets still oversupplied and commodity prices low, gas producer Chesapeake Energy plans to start cutting rigs and frac crews in March.