The Beast in the East will roar this year as the Marcellus reaches an inflection point. Bigger wells can fill the takeaway coming onstream. (Photography by: Glenn Kulbako)

A version of this story appears in the April 2018 edition of Oil and Gas Investor. Subscribe to the magazine here.

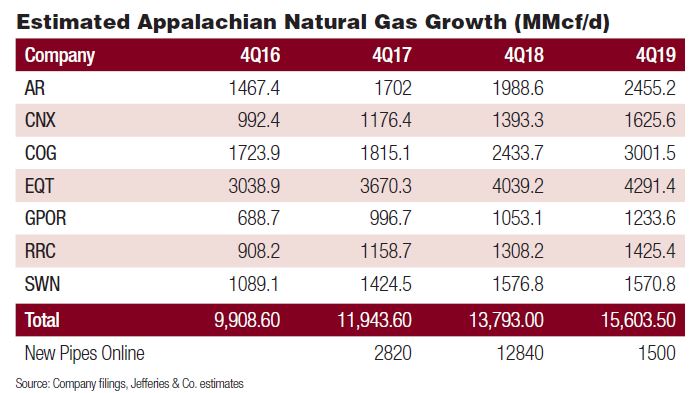

They call it the Beast in the East. Whether out of fear, envy or respect, U.S. natural gas producers worried about big gas supply and low prices regard the Marcellus Shale with awe thanks to its increasing production. Along with its fast-growing cousin, the Utica Shale, the Marcellus continues to dominate talk about U.S. gas production, exports and prices. Last year gas production growth from seven major shales was 9 billion cubic feet a day (Bcf/d), and the Northeast contributed about 37% of that increase (the Haynesville contributed 20%). Production in the region began accelerating in second-half 2017 in anticipation of more infrastructure coming online.

The Marcellus and Utica shales in Pennsylvania, Ohio and West Virginia were producing as much as 26.8 Bcf/d as of December 2017, nearly double what they produced in 2012, according to the latest figures from the U.S. Energy Information Administration (EIA). That’s more than a fourth of total U.S. production of 96.6 Bcf/d, and it is set to go higher. The EIA said Northeast dry gas production alone would be 23.5 Bcf/d in 2018—but that total could reach 35.6 Bcf/d by 2024. Well permits have risen in recent months.

But however prolific the geology here, well completions throughout the region are not being propelled by the allure of robust gas prices at Henry Hub, which at press time had declined 29% just since January. Realized prices as reported by numerous operators (not counting hedging) are below $3 and often below $2 per thousand cubic feet (Mcf). On the other hand, finding and development costs are some of the lowest of any gas play in the world, ranging from 22 cents to 40 cents per Mcf.

Seeing the prolific nature of the Marcellus, Utica and other gas plays, Bernstein Research analyst Jean Ann Salisbury has deemed 2018 “the year of the gas tsunami.” In a recent report she said, “We believe that 2018 will be the year we see gas supply really start to ramp up as associated gas grows and Marcellus pipelines finally come online. We expect gas to fall to $2.50/MMBtu [million British thermal units] or below by the middle of the year and stay there through 2020. This is 10%-plus below the forward curve.”

The rosy activity outlook in Appalachia is the result of better well results being recorded, coupled with improving gas demand. Drillbits will turn because this year, finally, several key infrastructure projects that producers have been counting on will come to fruition, and these need to be filled to meet firm volume commitments.

“We think that as an industry, we will fill that new pipeline capacity,” said Tim Dugan, COO of CNX Resources Corp. (NYSE: CNX). “It may not happen immediately, but it will get filled. With the onset of the dry gas Utica play developing in central Pennsylvania, plus the upper and lower Marcellus and Devonian, there are plenty of stacked pays. We think Appalachian production can grow by 4 Bcf/d over the next 12 to 18 months, what with the many stacked pays in the region, and more development of the dry gas Utica,” he told Investor.

Demand Arrives

Investors remain concerned that Appalachian Basin supply may outrun demand, but in March one of the biggest milestones for demand was reached when Dominion Energy Inc. started exporting LNG from its $4-billion Cove Point plant in Maryland. Cove Point can liquefy up to 750 MMcf/d. It will take gas supply from Royal Dutch Shell Plc (NYSE: RDS.A), which in turn will sell the LNG to utilities in India and Japan under 20-year contracts.

Even more in-basin demand is on the way. In December, Phase 1B of the Rover pipeline came onstream, with capacity to move 1.7 Bcf/d from Cadiz, Ohio, to Defiance, Ohio. Phase 2 is supposed to come online in the second quarter as well, said Energy Transfer Partners LP (NYSE: ETP). The Mariner 2 NGL pipeline will come on this year, and Mariner 2X will be on by mid-2019. Tied to these is ETP’s Revolution cryogenic processing plant in western Pennsylvania, which is supposed to be online this year to add an initial 200 MMcf/d of capacity, with the option to grow.

TransCanada Corp.’s (NYSE: TRP) Leach/Rayne Xpress projects began service in January, with anchor shippers including Range Resources Corp. (NYSE: RRC). EQT Corp.’s (NYSE: EQT) Mountain Valley pipeline, with firm capacity of 2 Bcf/d, is supposed to come on by year-end to move gas from West Virginia to southeast Virginia.

“Volumes historically sold in-basin will be ‘pulled’ from the basin by the new capacity coming online,” said Jefferies & Co. analyst Mark Lear in a January report, leading him to believe that local basis differentials will contract this year.

This June, two state-of-the-art power plants will start in Pennsylvania, both to be fueled exclusively by Cabot Oil & Gas Corp. (NYSE: COG) to the tune of an aggregate 405 MMcf/d from the company’s Susquehanna County production. At press time, Cabot announced it could grow gas production 35% this year on a divestiture-adjusted basis, using three rigs and two frack crews.

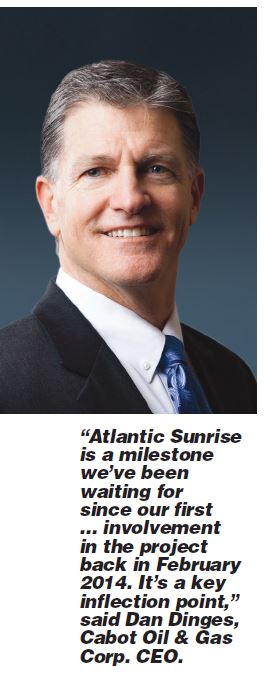

Once Transco’s Atlantic Sunrise pipeline goes onstream in the second half, it will take up to 1 Bcf/d of Cabot production from Susquehanna County to markets in the mid-Atlantic and Southeast. The path to this has been fraught: In November, courts granted protesters a temporary stay, halting construction, but in December, FERC refused to take up the matter and let its approval stand. Construction of the $3-billion line has resumed. Finally, once the PennEast Pipeline comes on in 2019, Cabot will ship 150 MMcf/d on that. Originating in northeast Pennsylvania, it will ship up to 1 Bcf/d to utilities in the southeast corner of the state and in New Jersey. FERC just gave its final approval in January.

You could almost hear a collective sigh of relief at Cabot’s Houston headquarters. The dominant operator in northeast Pennsylvania with 3,000 remaining locations, Cabot said it best in its updated February investor presentation: the last slide says “TEN-acious, a decade of progress and perseverance in the Marcellus Shale.”

“This is a milestone we’ve been waiting for since our first announcement and our involvement in the project back in February 2014,” said chairman and CEO Dan Dinges on the company’s February conference call. “It represents a key inflection point for the northeast Pennsylvania natural gas market and for Cabot. We continue to target a mid-2018 in-service for this project, on which we will be selling approximately 1 Bcf of gas to new markets.”

Production Pushes Ahead

Productivity for individual wells across the basin keeps improving with higher proppant loading, though gains are beginning to slow, according to Jefferies’ Lear. “In 2016, three-month ‘cums’ [cumulative production] per 1,000 feet have increased by 10%.”

He said limited state data available for full-year 2017 indicate proppant loading in Pennsylvania is now averaging 1,630 pounds per lateral foot, a clear boost to well productivity. On the other hand, he noted that 30-day IP rates in southwest Pennsylvania peaked at 9 MMcfe/d in first-quarter 2016 but have since trended down to 7 MMcfe/d as of first-quarter 2017.

“This may be the result of operators constraining wells initially in order to manage pressure in an effort to achieve longer ‘flat’ production,” he said.

Well productivity in northeast Pennsylvania does continue upward, with proppant loading there up 19% to average 1,830 pounds/foot. Six-month completion numbers are benefiting, he said in the report.

Every operator has guided to production increases this year and next. Cabot signaled a 2018 outlay of $800 million in order to drill 85 wells and complete 95. It figures finding and development costs of 22 cents/Mcf and all-in operating costs of $2.02/Mcf, (including operations, transportation and gathering, taxes, exploration, DD&A, G&A and interest).

Cabot’s Dinges said on the company conference call that Cabot’s growth in 2018 will be weighted toward the second half of the year due to the timing of new infrastructure in Pennsylvania, but its 2018 exit rate is expected to be 35% higher than the 2017 Marcellus production exit rate.

Longer term, Cabot’s Marcellus output can grow to 3.7 Bcf/d by 2020. It has 3,000 locations in inventory. “Despite peer-leading Marcellus EURs, expect further testing of new initiatives to further enhance EURs and economics … currently testing Gen-6 completion design,” said The Williams Capital Group’s Gabriele Sorbara in a report.

A worker checks the Centaurus CNG pressure reduction system at the CNX rig site.

With acreage stretching from eastern Ohio to southwest and central Pennsylvania and West Virginia, CNX is developing several plays and delineating the dry gas Utica, where it recently unveiled two huge wells. The company is now a pure play after shedding its coal assets and buying the 50% of its midstream entity it didn’t already own.

This year the company has guided to a 30% production increase in the Marcellus, to between 1.4 and 1.5 Bcfe/d, running three rigs now and possibly adding a fourth by midyear, Dugan said. Even though the company estimates a base decline rate of 32% annually, it expects production to go up from the 1.39 Bcfe/d it recorded last December. It plans to turn in line 46 new wells this year.

In 2017, CNX drilled a fairly even split of Marcellus and Utica wells, but this year it is drilling fewer Uticas, even though they have been highly successful. Why? CNX wants to delineate the dry Utica with what Dugan called a methodical approach. “We are continuing with data acquisition, but at the same time, the Marcellus in the near term will be our growth engine,” he said.

When the company acquired 50% of the [CONE Midstream] assets from Noble Energy Corp. (NYSE: NBL) and rewrote its gathering agreement, the deal included a pledge to drill 140 wells at a minimum in southwest Pennsylvania; the majority of them are in the Marcellus, he explained.

“But our enthusiasm for the deep dry Utica continues to grow: if anything, the data we’ve gotten strengthens our view.”

CNX’s 5J and 5M Aikens wells in Westmoreland County performed above the type curve of 3.5 Bcf per 1,000 feet. They each averaged 24 MMcf/d from dry gas Utica during their first 47 days.

“Our Aikens wells were the first pad drilling done in the dry Utica. Both were in the $15-million range, but the Gaut and GH9 wells that were drilled previously were $26- to $29 million for each one. So we’ve been able to drastically reduce our costs.

From the driller's console, the well can be safely monitored and drilled.

“The Utica plan is moving forward, and if anything could accelerate. I think we’ll be first to move into development mode in this Utica,” Dugan said. The company expected to release more detail at its analyst day in March.

A Parade Of Growth

Several other large Northeast gas producers likewise told investors to expect significant production growth from the Marcellus. Antero Resources Corp. (NYSE: AR) guided to a 20% production increase this year, to 2.7 Bcfe/d. It also signaled similar growth each year to 2020 (and as much as 24% from 2022 to 2024).

Its 2018 drilling and completion budget of $1.3 billion will cover the intent to drill 125 Marcellus and 25 Utica wells, with an average lateral length of 10,500 feet, although Antero continues to push technical boundaries. In fourth-quarter 2017, it drilled two Marcellus wells with lateral legs of 14,000 feet each, using 2,000 pounds of proppant per foot.

Southwestern Energy Co. (NYSE: SWN) cited 30% production growth in its southwest Appalachia footprint and 18% overall in Appalachia this year, with the capability to double production in the next four years with a fairly minimal $500- to $600 million annual spend, said CEO Bill Way on the company’s conference call. It plans to keep six rigs and five frack crews working.

The company expects to generate positive cash flow from operations, net of capital, for the first time in northeast Appalachia. It exited 2017 producing 2.35 Bcfe/d from its gross operated wells in the basin, a 40% increase from December 2016 rates and a record for the company.

Range Resources guided to 25% production growth in southwest Pennsylvania. Its first-quarter 2018 output was to be 2.1 Bcfe/d, about 30% NGL.

“We’re excited about what we see as we begin to harvest the top-tier inventory we’ve captured since discovering the Marcellus in 2004,” said CEO Jeff Ventura. “We expect to generate in southwest Pennsylvania growth of 25% in 2018, allowing us to fully utilize our transportation capacity,” he said on the company’s conference call.

All the robust production announcements by numerous operators, despite low gas prices, led Société Générale gas analyst Breanne Dougherty to say she is contemplating upward revisions to her 2018 U.S. gas profile—but at the same time, she has a softer price outlook of $2.77/Mcf for the year.

“Our current month-over-month production growth forecast for the remainder of 2018 averages 0.3 Bcf/d, in line with the average observed growth rate between January and October 2017,” she wrote in a recent report.

Raymond James analyst Darren Horowitz also sounded optimistic about production growth, and well before the recent slew of conference calls that detailed operators’ 2018 plans.

“In our cash-flow-driven model, we estimate a 30%-plus increase in Appalachian drilling activity from current levels of 65 rigs up to 87 by year-end 2018. Additionally, we expect a drawdown of the current DUC [drilled but uncompleted wells] backlog from about three months of a completion backlog to a more normalized level of two months by mid-2018.” At press time there were 56 rigs in the Marcellus and 21 in the Utica in Ohio.

“The combination of more drilling and even faster completions should translate to about a 10% increase in year-over-year average daily production volumes.” he wrote.

Tech Boundaries Fall

Operators continue to push the boundaries of technology by matching completion designs to the specific geology underneath each drill pad, all while reducing costs. EURs per 1,000 feet of pay have continued to climb. Longer laterals and more intense completions feature in every operator’s plans.

“Our completions have become very customized, based on what the drilling logs tell us,” CNX’s Dugan told Investor. “And, we’re using reservoir modeling with data analytics and machine learning, so we’re getting much better data than previously.”

Managed pressure drawdowns to protect the reservoir are a crucial component as well.

“Flowbacks are absolutely important,” Dugan said. “It became prominent when people started flowing these dry Utica wells … early on companies flowed these wells really hard and we saw several examples where they caused damage in the wellbore and had sand crushing in the fractures. Managed pressure drawdown and using the right transient analysis lets you understand how hard you can pull the well.

“We have seen fairly significant benefits in increasing the EURs and maintaining steady flow rates for a longer period of time by having a better understanding of the reservoir. Data analytics and machine learning has helped us understand this much better. It’s very important ... and critical in the higher-pressure Utica wells, but equally important in our Marcellus wells.”

Although managed drawdowns started in the Utica play, CNX plans to follow this practice increasingly in its Marcellus production as well, Dugan said.

Steve Schlotterbeck, EQT’s president and CEO, credited the company’s November 2017 megamerger with Rice Energy Inc. for some of the technical progress made. He said the deal has already led to better well results for EQT because best practices from each company are being integrated, as are the technical teams. In December 2017, the first full month of production after the merger closed, output reached 4 Bcfe/d.

“Initial development plans for our consolidated acreage target a 50% increase in average lateral length … resulting in a 40% reduction in per unit LOE [lease operating expense] and production SG&A expenses,” he said while commenting on 2017 results on the conference call.

The company’s Marcellus wells are expected to average 13,800 feet this year, or about 1,000 feet longer than what had been announced just a few months earlier. “This is a direct result of the collaboration between land professionals in both companies,” said senior vice president David Schlosser. EQT retained more than 150 Rice employees.

What’s more, EQT has some new bragging rights: It announced that it recently turned in line the longest lateral well completed to date by any operator in the Marcellus Shale. Its Haywood H18 well in Washington County has a completed lateral length of 17,400 feet and will develop 42 Bcfe of reserves, the company reported. Laterals of this length are projected to have development costs of $0.36/Mcfe. They will generate an internal rate of return greater than 70% at $3 gas. The company plans to drill 27 Marcellus wells at 17,000 feet or longer in 2018.

Thanks to technical advances, Southwestern Energy managed to double its Appalachian reserve base in 2017, but at a faster pace than it had three years ago, when gas prices were much higher. The gas price has fallen by $1.37/MMBtu since then—but the company is making more with less, just like all producers.

Tighter stage spacing, longer laterals and optimized well flows mean that new wells are outpacing historical offset wells drilled two and three years ago. This production uplift was in some cases better by 30% per lateral foot, according to Clay Carrell, Southwestern’s new executive vice president and COO, who joined the company in December.

Cabot said it will test a Gen-5 completion design on a few upper Marcellus wells in the second half of this year, with an estimated EUR of 2.9 Bcfe per 1,000 lateral feet drilled. Gen 5s are already tracking EURs of 4.4 Bcfe per 1,000 feet in the lower Marcellus, the company said on its conference call.

CNX Resources' green air compressors and boosters create air volume used when drilling, in addition to drilling mud. Any gas produced during drilling flows through the red pipe to be flared.

Range Resources Corp. COO Ray Walker announced that one well in its core southwest Pennsylvania acreage had a lateral of 17,875 feet and another well on the same pad will go to 18,100 feet horizontally this year.

Its southwest Pennsylvania wet gas wells with laterals averaging 9,550 feet generated EURs averaging 28 Bcfe per well. Its super-rich gas wells, meanwhile, had even larger EURs of 30 Bcfe and longer laterals of 11,550 feet. Optimized downspacing to 700 feet between wells yielded a 50% increase in cumulative production after 1,300 days, with no detrimental impact to the production of the original or parent wells, Walker said.

Change Agents

Several Appalachian companies have gone through big changes—or may do so this year. Many have said they will be cash-flow neutral or even cash-flow positive later this year, and certainly by 2019. Returning cash to shareholders is on tap for several of them, whether as dividends or stock buybacks.

But significant structural changes are taking place as well, as some of the companies are pressured by activist investors to take a closer look at the value of the sum of the parts. That is in part what drove last year’s EQT merger with Rice Energy to form the largest gas producer in the basin, and in the country. More recently, EQT said it is contemplating spinning off its EQT-Rice midstream entities into a new company later this year, possibly in September. Antero Resources is contemplating a move to consolidate its two public midstream entities.

Significant changes were made by CNX (formerly Consol Energy) last year. It “went live” in November as a pure-play E&P company, having spun off its coal business into a separate public entity. It also acquired the general partner of CNX Midstream, eliminating several midstream liabilities. Shareholders approved: through March, the company’s stock was up 9% vs. a peer average decline of 23%.

“We’re now a standalone E&P company, so our focus is on execution and operational issues,” COO Dugan said. “We really consider ourselves a capital allocation company with very good E&P assets.”

From those assets, CNX grew its total proved reserves at year-end 2017 to 7.6 Tcfe, a 21% increase from the prior year. Drilling and completion costs of $536 million facilitated turning 31 gross Marcellus wells to sales, with about 8,400 feet average lateral lengths. CNX reported improved EURs of 2.3 Bcfe per 1,000 foot lateral, vs. 2 Bcfe/1,000 feet in 2016.

Deep Dry Utica

In addition to heavily drilled northeast and southwest Pennsylvania and the West Virginia-Ohio area, increased drilling activity is extending the Marcellus and the deep dry gas Utica plays into other counties (Butler, Clarion, Westmoreland, Tioga and Indiana).

In the near term, the Marcellus will propel corporate production growth for CNX, but the company is also making hay in the dry gas Utica play unfolding in central Pennsylvania, where Dugan said he believes CNX has a first-mover advantage.

In this part of the Utica, CNX turned 22 gross dry gas wells to sales with laterals averaging 8,800 feet. It also increased type curves for PUD (proved undeveloped) reserves as a result, leading to the company booking 37% of Utica PUDs with EURs of 2.6 Bcfe per 1,000 feet of lateral (compared to 2.4 Bcfe/1,000 feet in 2016).

CNX announced two outstanding deep dry Utica wells there, the 5J and 5M Aikens in Westmoreland County. Using managed pressure drawdown with a restricted choke size, each well averaged 24 MMcf/d in the first 35 days, with an average flowing casing pressure of 8,672 psi. The company said it expects production from these high-pressure wells to be flat during the next 18 months, with cumulative production for both wells combined to be 2.43 Bcf during the same period.

The Aikens wells follow on the heels of CNX’s well-known Gaut 41H, announced in 2015 in Westmoreland County, which flowed 61 MMcf/d on a 24-hour IP. If one assumes the same EUR of 3.5 Bcfe per 1,000 feet of lateral as the Gaut, CNX said it expects average after-tax rates of return from the Aikens wells of approximately 50%.

“The 5J looks like it’s going to be the second-best well ever in this play—maybe the best gas well in the whole country--and second only to the Scott’s Run drilled a couple years ago by EQT,” Dugan told Investor. (That well tested 72.9 MMcf/d.)

“The Gaut was the second-best well drilled, but it looks like these two Aikens wells will surpass the Gaut,” he said.

Two more such wells will soon come on, one in Greene County; one in Indiana County, he said.

An important factor for capital efficiency and savings on gas processing is that the dry gas Utica production CNX has can be blended with wet Marcellus production, which by itself might be marginally economic in some areas, Dugan pointed out. Some of its acreage in southwest Pennsylvania straddles the wet gas-dry gas line, in areas producing what he calls “damp gas.”

“We take the dry Utica and blend it with damper gas and get the result down to pipeline quality gas. The gas is wet enough to require processing but the economics don’t justify it, but we can blend wet and dry and send that to a dry gas outlet, saving us the processing costs… You blend it at the right ratio to send it out through a dry outlet. I think we’re the only operator that has the infrastructure to blend like that and take advantage of these wetter areas.”

Dry gas is under 1,100 Btu, damp is 1,100 to about 1,250 Btu and beyond that, 1,250 Btu is considered to be wet gas with a lot of NGL that has to be extracted.

Any Caution Ahead?

Several producers and midstream experts working in the Northeast have sounded cautionary notes, despite the long-awaited midstream progress at hand. At Hart Energy’s annual Marcellus-Utica Midstream Conference in Pittsburgh in January, Crestwood Equity Partners’ (NYSE: CEQP) CEO Robert Phillips warned of future bottlenecks. He said that by the end of this year, even though several pipelines are set to come onstream, Marcellus production will soon surpass that added capacity, “leaving us right back where we were two or three years ago.”

Range Resources COO Ray Walker told analysts on his conference call, “… our internal work shows that when you look at the natural gas takeaway projects that have come into service since the third quarter of 2017, only about half of that volume is new gas, with the other half simply being local gas that was being displaced. More broadly, storage levels are likely to end the winter season between 1.4 and 1.5 Tcf, which will require a significant injection season to bring storage levels closer in line with the five-year average by the end of October.

“So, we think, like we’ve said for a long time, that there’s going to be ample pipeline takeaway gas capacity in the basin. It’s going to be overbuilt.”

If the lack of takeaway capacity is solved, and longer laterals and enhanced completions have led to much greater gas flows, then the next piece of the puzzle to solve is demand.

“We think demand pull will start occurring,” Walker said. “We already have a lot of that taking place. Even on the liquids side, it's beginning to take place where markets are actually coming to us to buy the gas at the tailgate of the Houston [Pennsylvania] plant, so to speak. So we see a lot of that shift beginning to take place, just like we predicted it would for years.”

Bernstein’s Salisbury warned that after the current 12-Bcf/d pipeline buildout in Appalachia is achieved, there may not be much need for incremental growth from the Marcellus “if this associated gas growth continues” from oily plays elsewhere such as in the Permian Basin. “There is little room left for growth from the non-oil-associated gas basins including the Marcellus, Haynesville, Fayetteville and non-condensate western Canada. This impacts E&Ps and midstream companies alike with focus there.”

Even so, FERC has a quorum now to begin deliberating on new takeaway projects in the region, although at the same time, public opposition continues to take its toll on company plans. Williams, Cabot Oil & Gas and the others behind the Constitution Pipeline recently asked the U.S. Supreme Court for help in their fight against New York State’s opposition to the line. New York has denied certain water quality permits associated with pipeline construction—blocking what could be a big pipeline taking Marcellus gas to New York and New England markets.

It’s never going to be easy to pursue development in the Northeast, even though the rock quality is outstanding and the technology being applied to it is incredible. Suffice it to say that the eyes of the world are watching how production totals advance over the next 24 months, how much gas is exported from the region to domestic and international markets, and how well the midstream sector can respond in kind.

Leslie Haines can be reached at lhaines@hartenergy.com.

Recommended Reading

Early Startup of Trans Mountain Pipeline Expansion Surprises Analysts

2024-04-04 - Analysts had expected the Trans Mountain Pipeline expansion to commence operations in June but the company said the system will begin shipping crude on May 1.

TC Energy's Keystone Oil Pipeline Offline Due to Operational Issues, Sources Say

2024-03-07 - TC Energy's Keystone oil pipeline is offline due to operational issues, cutting off a major conduit of Canadian oil to the U.S.

Waha NatGas Prices Go Negative

2024-03-14 - An Enterprise Partners executive said conditions make for a strong LNG export market at an industry lunch on March 14.

Enbridge Fortifies Dominant Role in Corpus Christi Crude Transport

2024-03-20 - Colin Gruending, Enbridge executive vice president and president for liquids pipelines told Hart Energy the company’s holdings in South Texas are akin to a “catcher’s mitt” for Permian and Haynesville production.

Squashing Midstream: Lessons Learned as Sector Looks to Horizon

2024-04-08 - What does the next level look like for the midstream sector?