Transocean’s Discoverer Deep Seas drillship is one of an estimated 47 floaters currently stacked—a number expected to continue rising. (Source: Transocean)

Optimism can be invaluable when times are tough, and boy do the rig market’s players need it right now. With most offshore rigs currently lying in the proverbial gutter, only the most wildly hopeful—to loosely quote Oscar Wilde—will be looking at the stars as 2016 passes them by.

It is indicative of how far the rig market’s star has fallen over the past year that several of the biggest contractors have even resorted to flagging up as “highlights” in their latest quarterly financial results that they have taken a client to arbitration over cancelled contracts.

The market is going through its most challenging period of the last 15 years and the lowest level of contracting activity seen since the 1980s. Oversupplied with multiple drilling rigs chasing very few opportunities, contractors face oil companies’ capex falling yet further this year after two prior consecutive years of decline, according to Norway’s Seadrill.

Overcommitted

“We continue to believe that the majority of rigs with contracts expiring in 2016 will be unable to find suitable follow-on work, many are likely to be idle for a protracted period, and consequently cold stacking and scrapping activity will accelerate. Oil companies continue to work on managing their existing rig capacity. They are in many cases overcommitted based on reduced activity levels, and there is very little appetite for adding new units,” Seadrill stated in its latest results presentation.

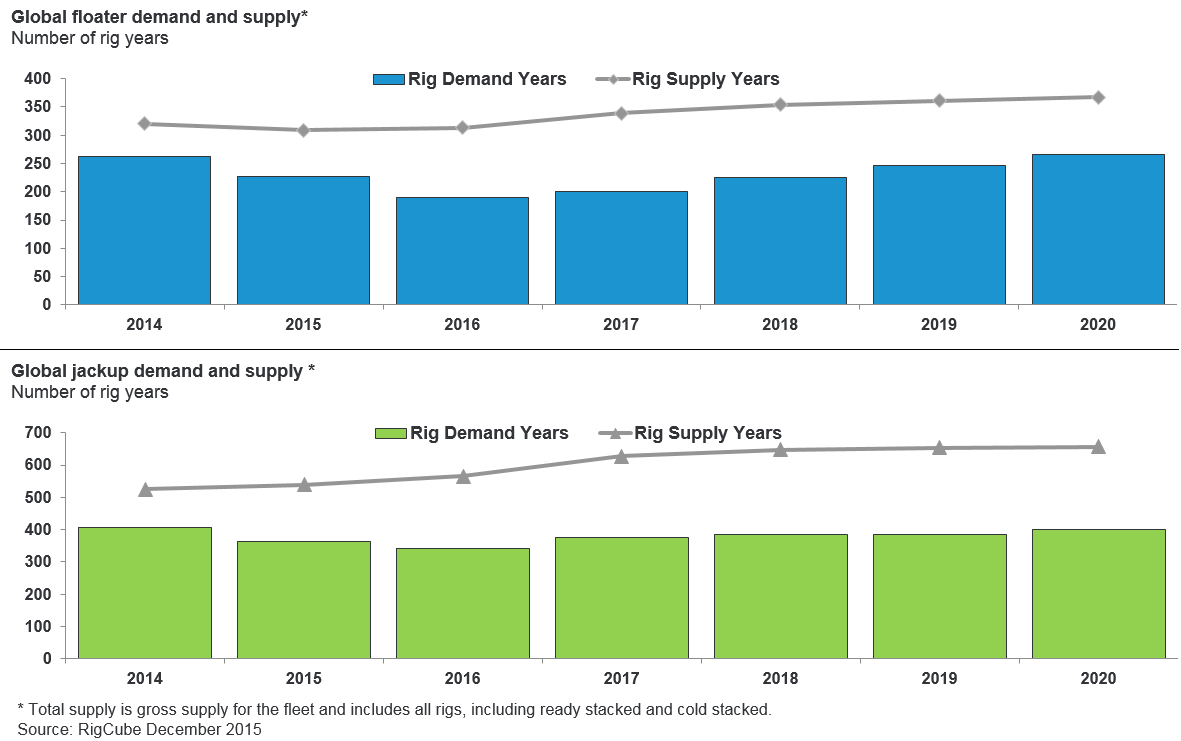

Analyst Rystad Energy agreed. It reported in January that the total global market dropped by up to 12% compared to 2014 levels. The floater market experienced the biggest fall with a 14% decrease in contracted rig supply in 2015, plunging from 262 units in 2014 to 227 units last year. The contracted jackup supply dropped by 11% last year, ending at 363 contracted rig years.

Contracted rig years from new contracts signed in 2015 amounted to 136 rig years (43.5 floater years and 92.5 jackup years), which is the lowest number over the past 15 years, while the low oil price and increased rig supply means day rates also have dropped significantly.

Day Rates Fall 40%

Latest new fixtures show average contracted day rates for floaters falling as low as $265,000, a drop of more than 40% compared to the 2014 average of about $450,000 per day. Jackup day rates also fell 40% from a 2014 average of $140,000 per day to $90,000 per day in fourth-quarter 2015.

Basically, 2016 is in the trough for the mobile offshore drilling unit (MODU) market, with a gradual recovery expected to start emerging in 2017, it said. According to Rystad’s forecast, the largest drop in activity this year will be in the floater market with a 16% decline from 2015. The global jackup market will suffer a smaller predicted fall of 6%.

Retirement Time

So what is being done to try to remedy the situation?

The focus in 2015 was increasingly on standing down older rigs, with 45 such retirements last year including 24 floaters and 21 jackups. The average retirement age in 2015 was 33 years, 32 for floaters and 35 for jackups, Rystad said.

But for the market to rebalance, there will need to be plenty more retirement activity combined with further action to delay the delivery of newbuild units from Southeast Asian shipyards.

One key factor in retirement decisions will be the timing of mandatory five-year surveys in relation to a rig’s specific contract status. “Rystad Energy sees no rationale for rig owners to undertake expensive surveys in the area of $50 million to $100 million unless the given MODU is on a contract or has a contract on the back of a survey,” Rystad commented.

Rebalancing

This rebalancing process should not be underestimated. According to deepwater specialist Ocean Rig, the floater fleet (marketed and cold-stacked) currently comprises 307 units, of which 149 were built prior to 2005—and which in reality are much older.

To rebalance the market, Ocean Rig said, the total floater fleet needs to be cut drastically to about 130 units from the current 307-strong fleet—not so much a cut as a complete decapitation.

Ocean Rig points out that the situation with Brazilian major Petrobras in particular has had a dramatic effect. The national oil company’s offshore rig fleet has declined from 70 units to about 40 at present, having previously accounted for about 30% of global demand.

The decline in drilling activity and the effect of the flood of newbuild rigs oversupplying the market (more than half of which did not have contracts lined up) was no great surprise, however.

According to McKinsey, the number of new contract fixtures globally has steadily declined since 2012, with 2013 fixtures being 25% lower and 2014 fixtures 50% lower compared to 2012. Last year simply continued that trend toward fewer contracts, with the oversupply further exacerbated by more than a quarter of contracts in place for existing rigs also expiring during 2015, leaving those units to compete with the arriving newbuilds and other existing idle rigs.

Rig Attrition

The biggest offshore driller, Transocean, has carried out and is carrying out actions typical of nearly all of its peers, including the cost-effective stacking of its ultradeepwater (UDW) floaters.

It also has been particularly vigorous in deferring the delivery of incoming newbuilds, with nine units currently on hold. According to Mark Mey, the company’s executive vice president and CFO, this level of rig attrition is key to the rebalancing of the market.

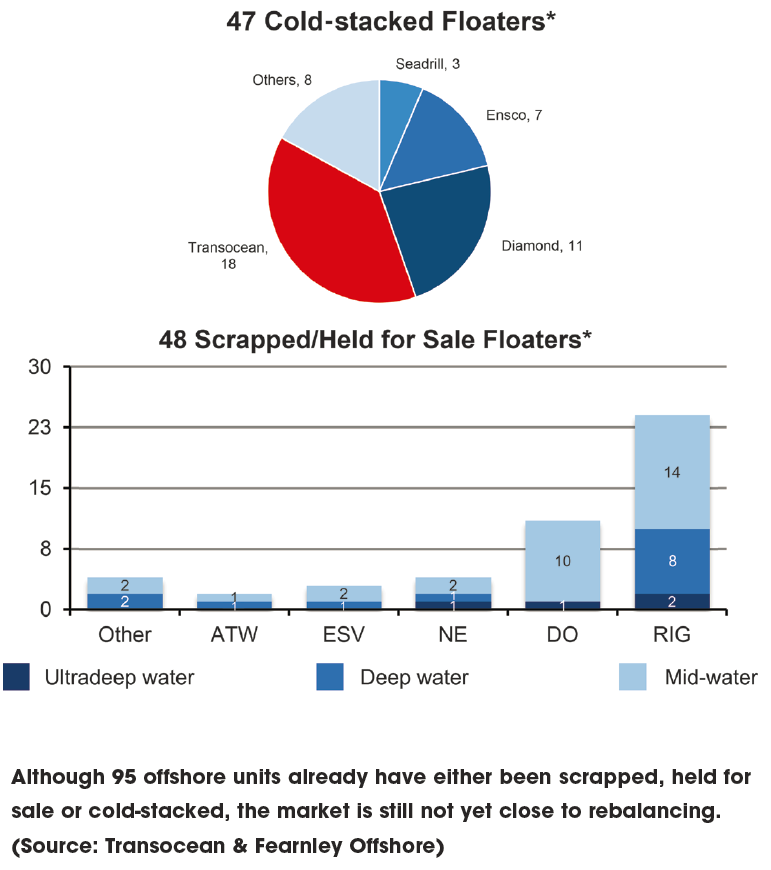

At present there are 47 cold-stacked floating rigs globally, with 48 more floaters either scrapped or held for sale. Transocean has 21 rigs stacked, with a further six currently idle, according to its latest fleet status report.

Transocean’s line of newbuilds is still out there, however. The company has 11 newbuilds in the pipeline between now and 2020—six UDW drillships and five high-specification jackups—representing about $6 billion of investment.

That compares to 19 newbuilds added by the company between 2009 and 2016—12 UDW drillships, three UDW semisubmersibles units and four high-specification jackups. These added up to a total investment of about $13 billion.

It has further cut its cloth to fit as recently as March, confirming a mutual agreement with Keppel Offshore & Marine’s shipyard, Keppel FELS, to defer the delivery and related payments of five high-specification jackups until 2020. The Super B 400 Bigfoot Class jackups are scheduled to be delivered in two- and three-month intervals beginning in first-quarter 2020.

The company also has suffered further cancellations this year, with Esso Exploration Angola (Block 15) Ltd. serving notice of early termination for the UDW semisubmersible GSF Development Driller I.

Murphy Oil was another that terminated a contract early, letting go the UDW drillship Discoverer Deep Seas, originally signed to work until November this year.

Plus Points

There also have been plus points already this year too with the company’s newbuild UDW drillship Deepwater Thalassa starting operations on its 10-year contract in the U.S. Gulf of Mexico at a day rate of $519,000. The rig, designed to operate in water depths of up to 3,658 m (12,000 ft) and drill wells to 12,192 m (40,000 ft), is another to feature Transocean’s patented dual-activity drilling technology and also its designed and patented Active Power Compensation hybrid system, plus a second BOP.

The drillship also is upgradeable to accommodate a 20,000-psi BOP system, the company said.

Transocean also reactivated its Henry Goodrich rig, which will now start a two-year contract offshore Canada at a day rate of $275,000 in second-quarter 2016.

The company’s experiences so far are typical of the sector as a whole. Ocean Rig, for example, has one harsh environment newbuild—the sixth-generation West Rigel semisubmersible unit—under a standstill agreement until June at Jurong Shipyard while it continues to try to land a contract for the unit.

The company has a further 11 units currently idle (five jackups and six floaters) and earlier this year also reached agreement with the Daewoo Shipbuilding and Marine Engineering yard to defer the delivery of two UDW drillships, the West Aquila and West Libra, until second-quarter 2018 and first-quarter 2019, respectively—with no further payments to the yard until delivery.

The company also is currently talking with China’s Dalian yard regarding the deferral of eight jackups there, with Ocean Rig not planning to take delivery of any units this year.

Distressed Assets

Such hard times can mean that other opportunities might emerge. Ocean Rig already has allocated $180 million to pursue distressed asset opportunities, forming an unrestricted subsidiary called Ocean Rig Investments to hunt down potential prey.

According to Rystad, 2016’s negative demand levels and day rates could spur merger and acquisition activity, distressed asset takeovers, and bankruptcies.

It’s an unforgiving market environment and one that is expected to play out throughout 2016, forcing rig companies to continue with their cold-stacking of idle units and the scrapping of older models until the rebalancing program is achieved.

Recommended Reading

NextEra Energy Dials Up Solar as Power Demand Grows

2024-04-23 - NextEra’s renewable energy arm added about 2,765 megawatts to its backlog in first-quarter 2024, marking its second-best quarter for renewables — and the best for solar and storage origination.

BCCK, Vision RNG Enter Clean Energy Partnership

2024-04-23 - BCCK will deliver two of its NiTech Single Tower Nitrogen Rejection Units (NRU) and amine systems to Vision RNG’s landfill gas processing sites in Seneca and Perry counties, Ohio.

Clean Energy Begins Operations at South Dakota RNG Facility

2024-04-23 - Clean Energy Fuels’ $26 million South Dakota RNG facility will supply fuel to commercial users such as UPS and Amazon.

Romito: Net Zero’s Costly Consequences, and Industry’s ‘Silver Bullet’

2024-04-22 - Decarbonization is generally considered a reasonable goal when presented within the context of a trend, as opposed to a regulatory absolute.